| Key Takeaways 1. Energy shocks are not black swans; they are repeatable market regimes that reward speed, not prediction. 2. Oil price direction, not headlines, sets equity outcomes—until energy stabilizes, broad markets stay fragile. 3. Futures markets are the earliest truth source, revealing risk shifts hours before cash equities react. 4. Energy and defense act as first-response profit centers, while airlines and consumers become immediate funding sources. 5. Correlation breakdown is the signal to rotate, not to diversify, making static portfolios structurally exposed. 6. The six-step blueprint is execution-driven: identify the oil breakout, confirm via futures, rotate capital immediately, hedge beta and volatility, ride the energy-led regime, and exit once oil momentum stalls—before consensus realizes the cycle has turned. |

Markets do not fear uncertainty; they fear sudden certainty delivered through force. When coordinated US and Israel strikes on Iran hit headlines, risk assets repriced before investors had time to debate narratives. This case study dissects how geopolitics, not earnings, seized control of global markets overnight.

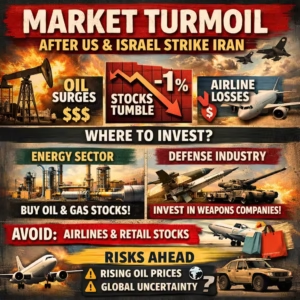

By 6:30 p.m. New York time, S&P 500 Index futures and Nasdaq 100 futures were down roughly 1%, signaling a decisive risk-off shift. Oil prices surged simultaneously, overriding diversification assumptions across portfolios. The opening shock exposed how fragile equity correlations become under geopolitical stress.

This episode reframes a hard truth for capital allocators. Energy and defense surfaced as tactical havens, while airlines and consumer sectors absorbed immediate drawdowns. Size, liquidity, and speed—not valuation—determined survival in the first hours.

The controversy lies in what failed. Traditional asset allocation models promised ballast, yet correlations collapsed when they were needed most. Geopolitics rewrote the market playbook before the opening bell.

For consultants and strategists, the lesson is blunt. Risk regimes change faster than consensus models adapt, and futures markets reveal that shift first. Ignoring them is no longer a defensible strategy.

Case Study Context: Sudden Geopolitical Escalation and the Risk-Off Market Regime

This case study centers on a direct geopolitical escalation involving the United States, Israel, and Iran. The immediacy of the action removed diplomatic ambiguity from market pricing. Risk was no longer theoretical; it was operational.

US equity-index futures reacted instantly. Near-1% declines before the cash open reflected institutional de-risking, not retail panic. Liquidity concentrated in futures markets amplified the signal globally.

Oil’s surge anchored the macro response. Energy became the dominant variable, overwhelming rate expectations and growth forecasts. Equity investors were forced into reactive positioning.

Sector dispersion widened within minutes. Defense and energy attracted inflows, while airlines and consumer discretionary saw indiscriminate selling. Correlation benefits evaporated under stress.

The regime shift was unmistakable. This was not a correction driven by fundamentals, but a shock driven by conflict. Markets repriced probability, not profitability.

Case Study Diagnosis: Market Mechanics Behind the Volatility Spike

Strategist insight clarifies the mechanics. Michael Kantrowitz of Piper Sandler & Co. notes that equities increasingly key off oil prices in geopolitical stress events. This linkage compresses reaction time across asset classes.

Oil acts as a transmission mechanism. Rising crude feeds inflation expectations, margin pressure, and valuation resets simultaneously. Equities struggle until energy prices stabilize.

Futures markets lead this adjustment. Price discovery now occurs before cash equities trade, leaving little room for discretionary interpretation. By the open, narratives chase prices, not the reverse.

Timing intensified the move. The shock hit during the Sunday evening US futures open, when liquidity is thinner. Small flows created outsized price signals.

The diagnosis is structural. Volatility was not accidental; it was engineered by market design. Understanding that design is now a strategic necessity.

Immediate Market Signals: Futures, Oil, and Sector Rotation

From our consultancy view point, this was not a “market surprise” — it was a failure of preparedness. The first signal was decisive and textbook: US equity-index futures dropped nearly 1%, a pre-cash alarm that only disciplined risk frameworks respect. Institutions that still debate signals at the cash open are structurally late; beta reduction must occur in futures, not in post-hoc equity trades.

Oil was the real governor of the tape, not headlines. The surge in energy prices immediately re-wired inflation expectations, forcing valuation compression across growth and consumer sectors. In our view, this is where most portfolios underperformed — they model oil as an input cost, not as a regime-setting variable.

Capital rotation was fast because it was rational, not emotional. Energy and defense absorbed inflows as short-duration shock absorbers, not long-term convictions. This distinction matters: tactical allocation wins crises, narrative investing loses them.

Airlines were structurally exposed, and the market punished them correctly. Fuel cost shock plus demand uncertainty created a double drawdown mechanism, while consumer discretionary cracked under confidence risk. These were not overreactions; they were forward-looking margin repricings.

The signal stack is where amateurs fail and professionals differentiate. Futures spoke first, oil validated the message, and sectors repriced accordingly. Miss that sequence and you’re not mis-timing the market — you’re misreading it entirely, which is why our consultancy treats futures and energy as first-order decision signals, not secondary indicators.

Root Causes: Why This Shock Transmitted So Fast

The geopolitical trigger was direct military action. Involvement of multiple state actors escalated tail risk instantly. Markets price escalation faster than resolution.

Energy sensitivity magnified the impact. Oil remains the dominant macro variable during conflict, cutting across regions and sectors. No alternative asset absorbed that shock fully.

Market structure accelerated transmission. Algorithmic trading and futures-led price discovery compressed reaction windows. Human discretion lagged machine execution.

Behavioral finance completed the loop. Flight-to-safety instincts triggered sell-first dynamics, regardless of fundamentals. Volatility fed on itself.

Speed was the root cause. The market moved because it could, not because it had finished thinking.

Sectoral Impact Map: Winners, Losers, and Second-Order Effects

Clear beneficiaries did not emerge—they were structurally inevitable, and this is where most investors misread the moment. Energy producers, oilfield services, and defense contractors were not trades of convenience; they were regime assets, and our consultancy treats them as such. When conflict drives pricing power, cash-flow visibility expands while multiples re-rate upward, and portfolios positioned early capture both beta and narrative dominance.

The losers were just as predictable, yet still crowded. Airlines were mathematically trapped by fuel cost pass-through limits, while consumer sectors faced an immediate collision between higher prices and weakening demand elasticity. Growth tech’s decline was not sentiment-driven—it was rate sensitivity resurfacing under an oil-led inflation shock, a nuance many missed.

Second-order effects are where our edge sharpens. Inflation-hedging flows were not defensive reactions; they were anticipatory reallocations, lifting commodities and TIPS as investors priced persistence, not spikes. Early credit spread widening signaled stress migrating from equities into balance-sheet risk, a warning most passive strategies ignore.

Volatility was not noise—it was information. Options and VIX-linked instruments became capital preservation tools, not speculative overlays, as liquidity premiums repriced in real time. The shift toward instruments with rapid exit capacity exposed a hard truth: liquidity itself became an asset class.

The asymmetry is the headline takeaway we emphasize to clients. Supply-side sectors captured upside through pricing power, while demand-driven sectors absorbed the shock through margin compression and volume risk. In geopolitical markets, neutrality is not diversification—it is underperformance by design.

USA Regional Lens – Texas & the Gulf Coast: Energy as a Strategic Hedge

Texas and the Gulf Coast became focal points. Concentration of upstream assets, refineries, and export terminals ties regional equities directly to oil spikes. Geography translated into portfolio defense.

Energy infrastructure mattered more than branding. Midstream stability and upstream leverage differentiated winners within the region. Capital favored operational resilience.

Employment effects followed capital flows. Energy-linked hiring and overtime expanded, offsetting national risk-off sentiment locally. Regional confidence held firmer.

Capital expenditure cycles adjusted upward. Producers revisited drilling and service contracts under improved price assumptions. Multiples expanded selectively.

The regional lesson is strategic. Energy geography functions as a hedge during geopolitical stress, not merely a sector bet.

USA Regional Lens – New York & Wall Street: Futures, Liquidity, and Price Discovery

On the Sunday evening futures open in New York, one large multi-strategy fund hit internal VAR limits within the first 18 minutes of trading as S&P 500 and Nasdaq 100 futures slid toward the 1% mark. Risk systems auto-triggered position reductions before portfolio managers had full geopolitical briefings, forcing index futures sales into thin liquidity. By the time human decision-makers were aligned, the price signal was already set.

On the floor and across prime broker desks, the reaction was procedural, not interpretive. Margin utilization alerts went out before analyst notes existed, and several equity long-short books cut gross exposure simply to stay compliant. Cash desks walked in Monday morning inheriting a futures-defined narrative they didn’t author.

Options desks felt the dislocation immediately. Overnight demand for index puts repriced protection sharply higher, widening bid-ask spreads and making hedging materially more expensive within hours. Traders weren’t hedging views; they were hedging mandates.

The anecdote exposes Wall Street’s real function in shock events. New York Stock Exchange doesn’t debate geopolitics first—it enforces risk constraints first. In practice, price discovery happens while explanations are still being drafted.

When futures, VAR models, and margin rules move first, Wall Street doesn’t “react” to geopolitics—it mechanically enforces the outcome before anyone has time to form an opinion.

PESTEL Analysis: Why This Event Matters Strategically

Political risk surged first. Military escalation elevated sanctions and sovereign risk across regions. Policy uncertainty became investable risk.

Economic pressure followed oil. Inflation risk tightened financial conditions, weighing on equities until energy stabilized. Growth assumptions reset.

Social confidence weakened. Consumers react quickly to energy price spikes, delaying discretionary spending. Sentiment erosion compounded losses.

Technology accelerated everything. Algorithmic and high-frequency trading shortened feedback loops. Speed replaced deliberation.

Environmental and legal layers resurfaced. Energy supply risk refocused attention on fossil fuel dependence, while compliance and sanctions exposure constrained cross-border trade.

Strategic Options: Portfolio and Corporate Responses

Tactical hedging moved to the forefront. Energy exposure and selective defense allocation reduced drawdown severity. Precision mattered more than scale.

Risk management turned dynamic. Futures and volatility instruments enabled rapid beta control. Static hedges underperformed.

Corporates faced operational decisions. Airlines revisited fuel hedging, while consumer firms reassessed pricing strategies. Execution speed defined outcomes.

Capital structure discipline gained importance. Liquidity buffers reassured investors amid widening spreads. Balance sheets became signals.

Strategy shifted from prediction to preparation. Flexibility outperformed conviction.

Immediate Market Shock: Risk-Off Repricing

Futures decline versus oil surge following sudden geopolitical escalation

Percentage moves reflect immediate post-event futures, sector, and commodity reactions.

Prevention & Mitigation: Reducing Exposure to Future Shock Events

Diversification needed recalibration. Single-factor macro dependencies, especially oil, required explicit stress testing. Assumptions were no longer implicit.

Scenario analysis expanded. Geopolitical plus energy shock models replaced isolated risk frameworks. Correlation breakdowns were baked in.

Monitoring became real-time. Futures and commodities served as early-warning indicators. Delayed signals proved costly.

Governance adapted. Faster decision rights reduced response lag. Committees optimized for speed, not consensus.

Mitigation favored readiness. The goal shifted from avoiding shocks to absorbing them.

Consultancy Takeaway: Turning Volatility into Competitive Advantage

This case study converges on a clear framework. Anticipate oil-led regimes, align sector exposure early, and manage liquidity at the futures signal stage. Strategy begins before the open.

The core insight is non-negotiable. Equities remain under pressure until oil prices stop rising, regardless of narratives. Energy dictates tempo in crisis markets.

Competitive advantage comes from structure. Firms that integrate geopolitical triggers into market mechanics act first. In volatility, speed is strategy.

At L-Impact Solutions, our view is simple and direct: geopolitics now moves markets faster than fundamentals. When oil spikes, diversification breaks, and waiting for clarity becomes a liability, not a strategy. The edge today isn’t prediction—it’s reading futures early, respecting energy as the lead variable, and acting before consensus catches up.

Reference – https://www.bloomberg.com/news/