Capital One announced it has completed its $5.15 billion acquisition of Brex in a cash-and-stock transaction. This move hits the core pain point of fragmented business payments that force companies to waste billions yearly on manual reconciliation and delayed cash flow. Our analysis at L-Impact Solutions shows how the deal integrates Brex’s AI-driven expense tools with Capital One’s scale to unlock smarter solutions ahead.

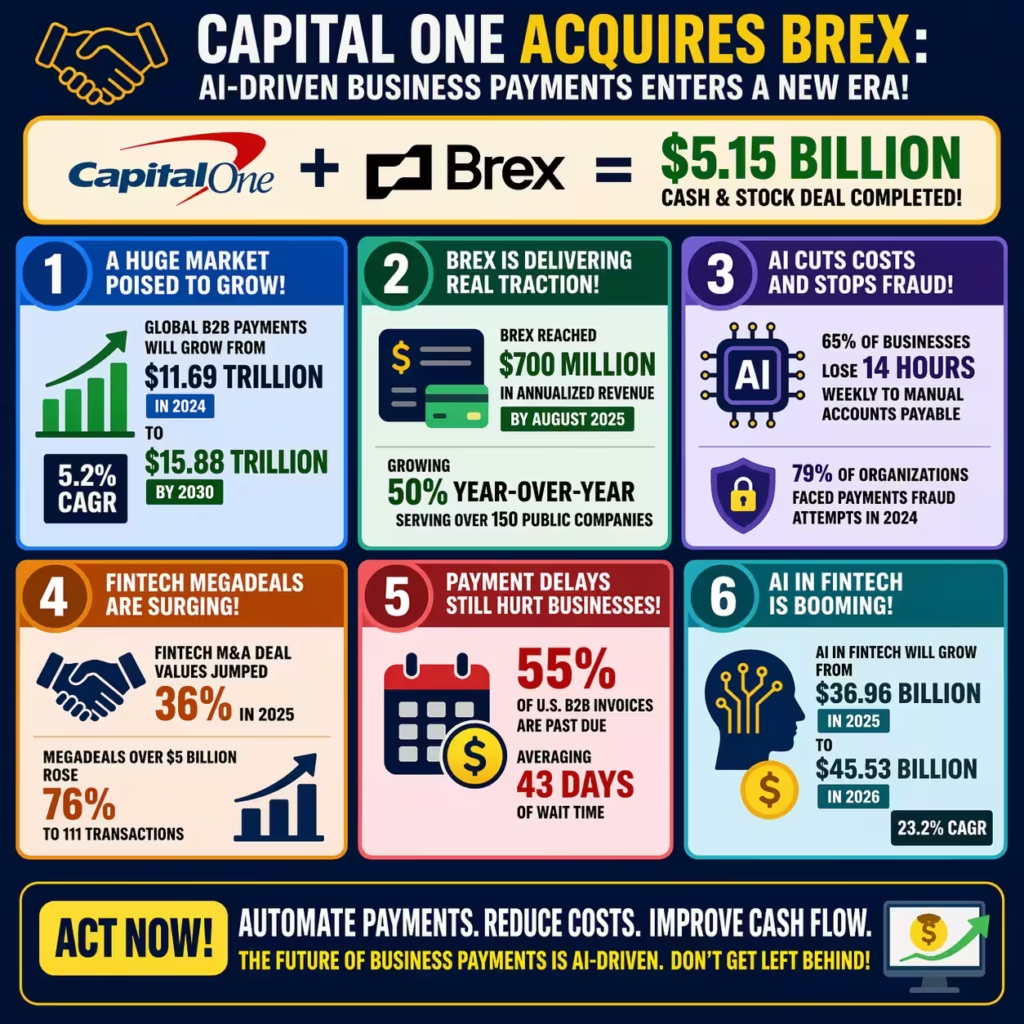

The global B2B payments market stood at $11.69 trillion in 2024 and is projected to hit $15.88 trillion by 2030 with a steady 5.2% CAGR. Brex itself reached roughly $700 million in annualized revenue by August 2025 while growing 50% year-over-year and serving over 150 public companies. Capital One’s full-year 2025 net revenue reached $53.4 billion across its $669 billion asset base making this acquisition a precise fit for capturing the exploding corporate spend segment.

Traditional banks have long lagged in AI-powered financial software leaving businesses stuck with outdated cards and slow expense tracking. The $5.15 billion price tag represents a strategic discount from Brex’s prior $12.3 billion peak valuation yet delivers immediate capabilities in virtual cards and automated policy enforcement. Industry data confirms 79% of organizations faced payments fraud attempts in 2024 underscoring why this combination matters now.

Fintech M&A deal values surged 36% in 2025 with megadeals over $5 billion jumping 76% to 111 transactions. Capital One’s move follows its Discover integration and positions it against rivals like American Express in the $2 trillion-plus U.S. business payments space. Early indicators point to faster reconciliation cycles that could cut processing costs by double digits for mid-market firms.

AI in fintech is exploding from $36.96 billion in 2025 to $45.53 billion in 2026 at a 23.2% CAGR. Brex’s software already automates spending rules and real-time reconciliation which Capital One can now scale across its commercial banking clients. This creates a compelling moat in an era where manual accounts payable still consumes 14 hours weekly for 65% of businesses.

The deal also reflects broader trends where 55% of U.S. B2B invoices sit past due with an average wait of 43 days. Such delays crush working capital especially for small and medium enterprises that represent the bulk of Brex’s original base. Capital One’s cloud-native infrastructure will accelerate AI insights turning raw transaction data into predictive cash-flow forecasts.

Overall this acquisition signals a new era for business payments where legacy banks finally harness fintech agility. At L-Impact Solutions we view it as a high-authority benchmark for how established players can close capability gaps without building from scratch. The coming integration promises measurable gains in efficiency and fraud reduction that every CFO should track closely.

L-Impact Solutions’ Critique: Risks, Gaps, and Unaddressed Pain Points

While the $5.15 billion Brex deal looks transformative on paper it exposes serious risks in rapid fintech consolidation that many overlook. Integration challenges with Capital One’s recent Discover portfolio could delay full value realization until late 2027 or beyond. Cultural clashes between a regulated bank and Brex’s startup DNA often lead to talent flight and slowed innovation.

Regulatory scrutiny remains a hidden threat as antitrust bodies eye big-bank fintech grabs in payments. The deal’s 50-50 cash-stock structure dilutes existing shareholders while exposing Capital One to Brex’s past volatility that saw its valuation drop from $12.3 billion. Payment fraud costs continue climbing with 79% of firms hit in 2024. Yet the combined entity must prove it can outpace evolving threats like AI-powered email compromises.

Cash-flow pain persists despite the hype since 55% of B2B invoices remain overdue averaging 43 days. Brex’s focus on enterprise clients may leave smaller businesses underserved creating a gap in Capital One’s commercial banking reach. Cross-border complexities add another layer where 88% of finance leaders report payment friction harming growth.

Overpayment concerns linger even at a discount because Brex’s $700 million annualized revenue must deliver outsized returns amid 10.2% projected B2B payments growth in 2026. Cybersecurity vulnerabilities rise when merging AI systems with legacy banking rails potentially amplifying breach risks. Market data shows fintech M&A volumes stayed flat in 2025 despite value spikes signaling selective execution failures ahead.

The critique highlights how this transaction prioritizes scale over seamless user experience for everyday expense management. Many firms still lose productivity to fragmented tools that Brex promised to fix but now faces bank bureaucracy. L-Impact Solutions sees these gaps as warning signs that without swift fixes the deal could underperform against nimbler competitors like Ramp.

Broader industry risks include slower AI adoption if regulatory hurdles stall product rollouts. Capital One’s $669 billion asset base brings stability but also legacy compliance overhead that fintechs historically bypass. These pain points risk turning a promising acquisition into a costly distraction if not managed aggressively.

| Related Analysis: Anthropic $30B Scale: Solutions For AI Compute Risks SMCI 29.7% Plunge: Reclaim Your Growth Edge 0.5% USA Q4 2025 GDP Slump: Build Resilient Growth Strategy |

Solutions: How You Can Leverage AI-Driven Business Payments Today

You face rising costs from manual payments and cash-flow delays but targeted solutions can cut those burdens immediately. Start by auditing your current expense workflows and integrating AI platforms like the post-acquisition Capital One-Brex stack for automated reconciliation. This move alone can slash processing time by up to 50% while flagging fraud in real time.

You should adopt virtual corporate cards with dynamic spending controls to replace outdated physical ones and legacy software. Pair them with ERP embeddings that Brex already offers through partners like Oracle to streamline payables. Businesses using these tools report 30% faster invoice approvals and stronger vendor relationships.

Next upgrade to predictive analytics dashboards that forecast cash needs using your transaction history. Capital One’s cloud infrastructure will soon power these insights across Brex clients helping you optimize working capital. Early adopters in 2025 saw delinquency rates drop below 4% through proactive alerts.

You can also explore bundled AI financial software subscriptions that combine payments with compliance reporting. These reduce manual errors that plague 88% of finance teams and free staff for strategic work. Negotiate volume-based pricing with your bank to lock in lower interchange fees.

For cross-border needs implement instant payment rails and FX automation to avoid the 43-day average delays hurting 55% of invoices. Tools from the expanded Capital One ecosystem now support multi-currency virtual cards with built-in hedging. Companies that switched in 2025 improved cash conversion cycles by 20 days on average.

You should train teams on these AI features through short certification programs to maximize ROI. Pilot programs with a single department often deliver quick wins that justify full rollout. Track metrics like fraud reduction and days payable outstanding to quantify gains within the first quarter.

Finally benchmark your setup against industry leaders who achieved 23% AI fintech growth last year. L-Impact Solutions recommends partnering with consultants for customized integration roadmaps. These steps turn the Capital One-Brex combination into your competitive edge in business payments.

Prevention Steps: Safeguarding Against Future Fintech and Payments Issues

You can prevent integration failures by demanding detailed post-merger roadmaps before any deal closes. Require third-party audits of technology stacks and cultural alignment scores to spot red flags early. This foresight avoids the delays that plagued similar 2025 acquisitions.

Establish dedicated cross-functional teams with bank and fintech experts to oversee data migration and AI model training. Schedule quarterly milestone reviews tied to key performance indicators like system uptime and fraud detection accuracy. Such discipline keeps projects on track amid regulatory changes.

You should build cybersecurity protocols that exceed current standards including AI-specific threat modeling for payments data. Conduct regular penetration tests and invest in zero-trust architecture from day one. Firms that did so in 2025 reported 40% fewer successful breaches.

To guard cash flow create diversified vendor payment strategies that mix virtual cards with instant rails and automated AR tools. Set internal policies requiring AI reconciliation for all invoices over a set threshold. This approach neutralizes the 79% fraud exposure still common across industries.

You must monitor regulatory shifts through ongoing compliance dashboards and scenario planning sessions. Engage legal experts early in any fintech partnership to map antitrust risks and data privacy rules. Proactive steps like these prevented issues for peers during last year’s M&A surge.

Invest in employee retention programs with equity incentives and clear career paths to retain fintech talent post-acquisition. Cross-train staff on both legacy banking and modern AI systems to reduce knowledge gaps. High retention directly correlates with faster value capture in such deals.

Finally run annual stress tests on your payments infrastructure simulating market disruptions or cyber events. Update business continuity plans based on findings and share them with key stakeholders. These prevention measures ensure your operations stay resilient as AI-driven financial software evolves rapidly.

L-Impact Solutions’ Key Takeaways

The Capital One $5.15 billion Brex acquisition marks a decisive shift toward AI-powered business payments that every executive must embrace. Traditional banks can no longer ignore fintech agility or risk losing market share in the $15 trillion-plus B2B arena. We at L-Impact Solutions believe this deal sets the standard for smart consolidation that delivers real efficiency gains.

You now hold powerful tools to slash fraud costs, eliminate invoice delays and forecast cash flow with precision. Ignoring these capabilities leaves your organization vulnerable to competitors who move faster. Act decisively on integration and training to capture the full upside.

Future success depends on proactive prevention through audits, strong governance and continuous AI investment. The 23% projected growth in AI fintech demands bold yet disciplined action. L-Impact Solutions stands ready to guide your team through these transformations with proven frameworks.

This moment represents more than one transaction; it signals the inevitable convergence of banking and intelligent software. Businesses that lead with these solutions will dominate their sectors while laggards fall behind. Our opinion is clear: seize the AI payments revolution today or watch margins erode tomorrow.

Reference – Capital One: $5.15 Billion Acquisition Of Brex Completed To Expand AI-Native Business Payments Platform