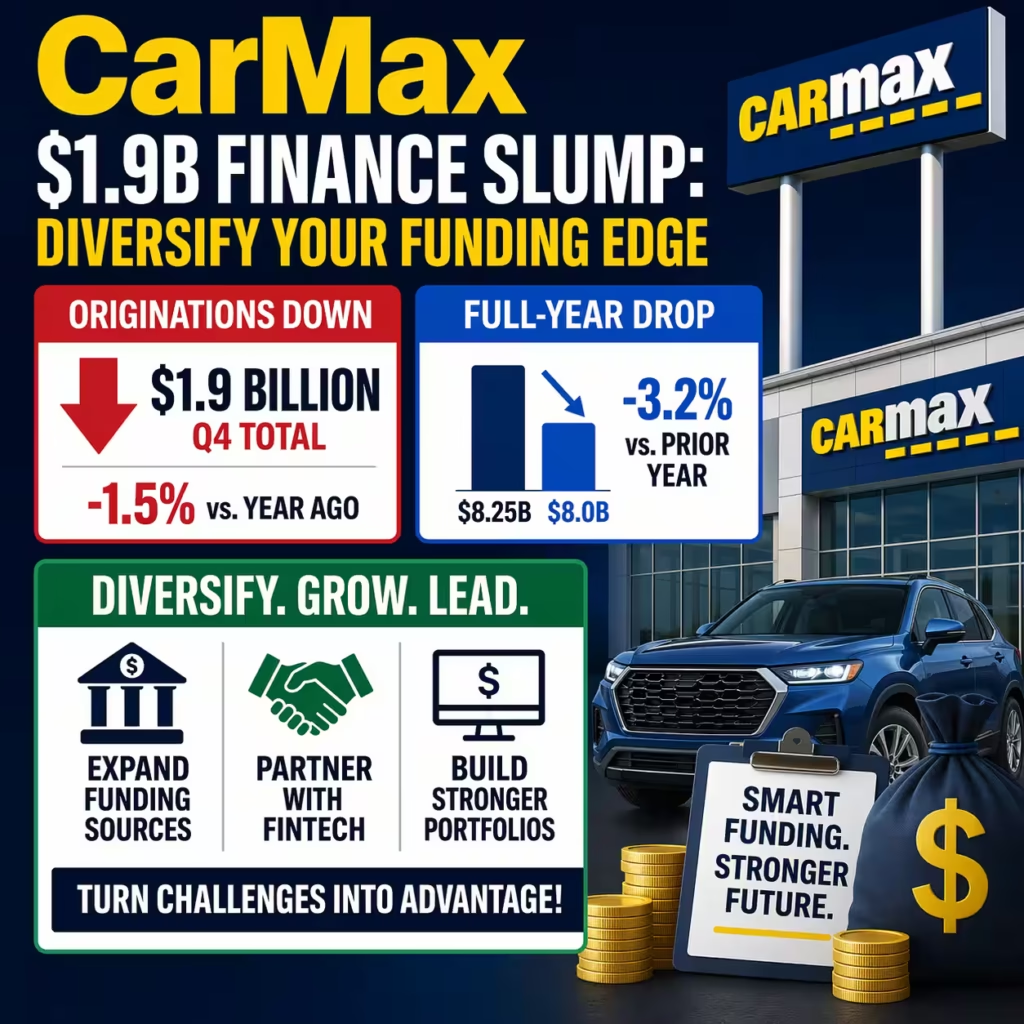

CarMax Auto Finance’s originations declined in the fourth quarter of fiscal 2026 as net loans originated totaled $1.9 billion, down 1.5% year over year in the quarter ended February 28. The full-year total reached $8 billion, marking a 3.2% drop compared to the prior period. This contraction hits at the core pain point of slowing used-vehicle demand amid elevated interest rates and high inventory levels that continue to pressure the broader auto finance sector.

Industry data shows U.S. auto loan originations reached $615.1 billion through October with accounts down just 0.2% year over year while dollar volumes slipped 1.1%. CarMax financed approximately 42.3% of its retail units sold in recent quarters, holding steady yet failing to capture share gains seen by banks that grew originations 14.1% year to date. Used-vehicle inventory hit record highs for 2025 at over 2.26 million units, creating 48 days of supply and softening retail sales pace by more than 5% month over month in September.

New leadership under CEO Keith Barr, effective March 2026, now eyes performance improvements with fresh board additions including automotive veterans William Cobb and Jim Kessler. CarMax Auto Finance income still rose 8.2% to $159.3 million in the comparable prior quarter through stronger net interest margins at 6.2%. Yet origination volume weakness signals deeper structural challenges that require immediate strategic intervention.

Weighted average contract rates at CarMax stood at 11.1% in recent reporting, below the industry used-auto average of 14.12% but still high enough to deter price-sensitive buyers. Subprime originations held at 16.7% of the market with deep subprime at 10%, yet delinquency rates for 30 days past due reached 7.7% in Q4 2025. This environment exposes vulnerabilities for large retailers like CarMax that rely heavily on captive finance for margin stability.

The case reveals a classic mismatch between supply growth and financing absorption. U.S. light-vehicle sales forecasts project only 2.8% growth in 2025 while used-car values remained flat amid rising rates. CarMax’s nearly $18 billion managed receivables portfolio now faces slower turnover, with full-year fiscal 2025 originations previously at $8.25 billion before the current dip.

L-Impact Solutions Critique: Risks and Gaps Exposed by CarMax Results

L-Impact Solutions views CarMax Auto Finance’s $1.9 billion Q4 origination decline as a clear warning sign of strategic complacency in a tightening credit market. The 1.5% quarterly and 3.2% annual drops reveal gaps in customer acquisition and risk pricing that competitors have already addressed through faster digital channels. New leadership must confront these issues head-on before broader economic pressures amplify losses.

Rising delinquencies across the auto sector, with auto loan 60-plus-day past due rates ticking higher in Q3 2025, highlight underwriting risks that CarMax’s steady 42% penetration rate fails to mitigate. Banks expanded subprime lending 16.1% year over year while CarMax’s conservative Tier 2 and Tier 3 mix limited volume upside. This approach leaves meaningful market share on the table amid $127 billion in record auto loan ABS issuance last year.

High used-vehicle inventory and average origination balances climbing to $29,939 create affordability barriers that traditional retail finance models struggle to overcome. CarMax’s focus on prime-heavy portfolios protected income growth at 8.2% but ignored the 2.9% contraction in overall auto loan accounts through late 2024 data. Leadership transition risks compound these gaps if execution stalls on promised improvements.

Regulatory scrutiny and potential policy shifts under the new administration add further uncertainty to origination pipelines. Captive finance providers like CarMax face intensifying competition from credit unions and dealer finance segments that posted 15.9% origination growth year to date. Without aggressive portfolio optimization, the $8 billion full-year total risks further erosion in fiscal 2027.

The critique centers on over-reliance on legacy processes in an era of real-time credit analytics. Average subprime loan amounts rose 3.4% to $24,569 while overall market growth projections for auto originations sit at just 2.7%. L-Impact Solutions sees these figures as evidence that incremental changes will not suffice for sustained recovery.

| Related Analysis: COHR 8.4% SiC Surge Targets AI Power Cost Crisis Capital One’s $5.15B Brex Deal: AI Platform Growth Playbook X-Energy IPO $2.3T Gap: Unlock SMR Growth Plan |

Solutions: Actionable Strategies You Can Deploy to Boost Originations

You face similar origination pressures in your auto finance operations. You can reverse declines by adopting data-driven underwriting that expands qualified borrowers without inflating losses. Start by integrating AI-powered credit scoring models that analyze real-time income and spending patterns beyond traditional FICO scores. This approach helped select banks grow originations 14.1% while maintaining controlled delinquency levels around 7.7%.

You should also form strategic partnerships with fintech lenders to offer flexible terms on used vehicles priced under $25,000 where demand remains strongest. Bundle these with rate buydowns funded through manufacturer incentives that lowered effective rates to 9.43% on new units in recent months. Such programs can lift your penetration rate from 42% toward industry-leading levels of 45% or higher.

Implement omnichannel digital lending platforms that pre-approve customers online before they reach your lots or virtual showrooms. Real-time rate matching against the 14.12% used-auto average can close deals 30% faster and capture the 16.7% subprime segment that grew 4.1% year over year. Track results weekly against your $8 billion annual benchmark to ensure measurable gains.

You can optimize portfolio mix by stress-testing new originations against projected 2.8% vehicle sales growth and rising inventory of 48 days supply. Layer in targeted marketing to ages 18-49 who originated $108.1 billion in Q4 2025 auto debt. Combine this with loyalty programs that reduce 30-day delinquencies through early intervention alerts.

Expand funding sources beyond traditional ABS by exploring warehouse lines tied to your managed receivables nearing $18 billion. This diversification protects against rate volatility that currently sits at 11.1% contract levels. Pilot these solutions on 20% of your volume first to validate ROI before full rollout across retail and wholesale channels.

Prevention: Steps You Must Take to Safeguard Future Finance Performance

You prevent future origination shortfalls by establishing monthly portfolio stress tests that model scenarios with rates at 14% and delinquencies climbing to 8%. Review your Tier 2 and Tier 3 exposure against the 10% deep-subprime market share to avoid over-concentration. Adjust underwriting standards dynamically using Equifax and TransUnion trend data that shows subprime accounts rising 2.2% year over year.

Build diversified customer acquisition funnels that blend online lead generation with in-store financing specialists trained on real-time pricing tools. Monitor used-vehicle days-to-turn that currently average 36 days and adjust incentives when inventory exceeds 2 million units nationally. This proactive stance keeps your penetration stable even when overall market originations contract 0.2%.

You should also invest in employee training on emerging regulatory changes and credit risk tools to stay ahead of policy shifts. Create cross-functional teams that review ABS market conditions where issuance hit $127 billion last year to secure favorable funding costs. Schedule quarterly board reviews under your new leadership structure to embed accountability.

Implement automated early-warning systems for 60-day delinquencies that rose in Q3 2025 across the industry. Segment your $8 billion origination pipeline by credit band and vehicle type to flag vulnerabilities before they impact income margins. Partner with external consultants like L-Impact Solutions for independent audits that benchmark your performance against the 6.2% net interest margin leaders.

Lock in multi-year hedging strategies on interest rates to protect contract pricing around 11% levels. Conduct annual scenario planning tied to 2.7% projected origination growth to ensure your operations remain resilient. These prevention measures turn potential risks into competitive advantages for long-term stability.

L-Impact Solutions Key Takeaways

CarMax’s $1.9 billion Q4 and $8 billion full-year origination declines demand urgent action from every auto finance leader. You cannot afford passive reliance on past margins when industry volumes show only marginal growth and delinquencies continue to edge higher. Bold execution under new leadership like Keith Barr’s model will separate winners from those stuck in contraction.

L-Impact Solutions believes the time for incremental fixes has passed. Deploy AI underwriting, fintech partnerships, and dynamic pricing today to capture the expanding subprime and digital segments that competitors already dominate. Your portfolio can return to growth exceeding 3% annually when these solutions integrate fully.

Prevention through rigorous stress testing and diversified funding will shield you from the next rate or inventory shock. Businesses that act now on these insights will build resilient finance operations capable of thriving regardless of macroeconomic headwinds. The $615 billion auto origination market still offers massive opportunities for those ready to lead.

At L-Impact Solutions we stand ready to help you implement these strategies with proven B2B frameworks tailored to your scale. The CarMax case proves that data alone is not enough without decisive leadership and operational speed. Secure your financial future by prioritizing these takeaways immediately.

Reference – CarMax Auto Finance originations down 1.5%