SanDisk’s $2.6B AI storage growth highlights the need for efficient, scalable data orchestration strategies today.

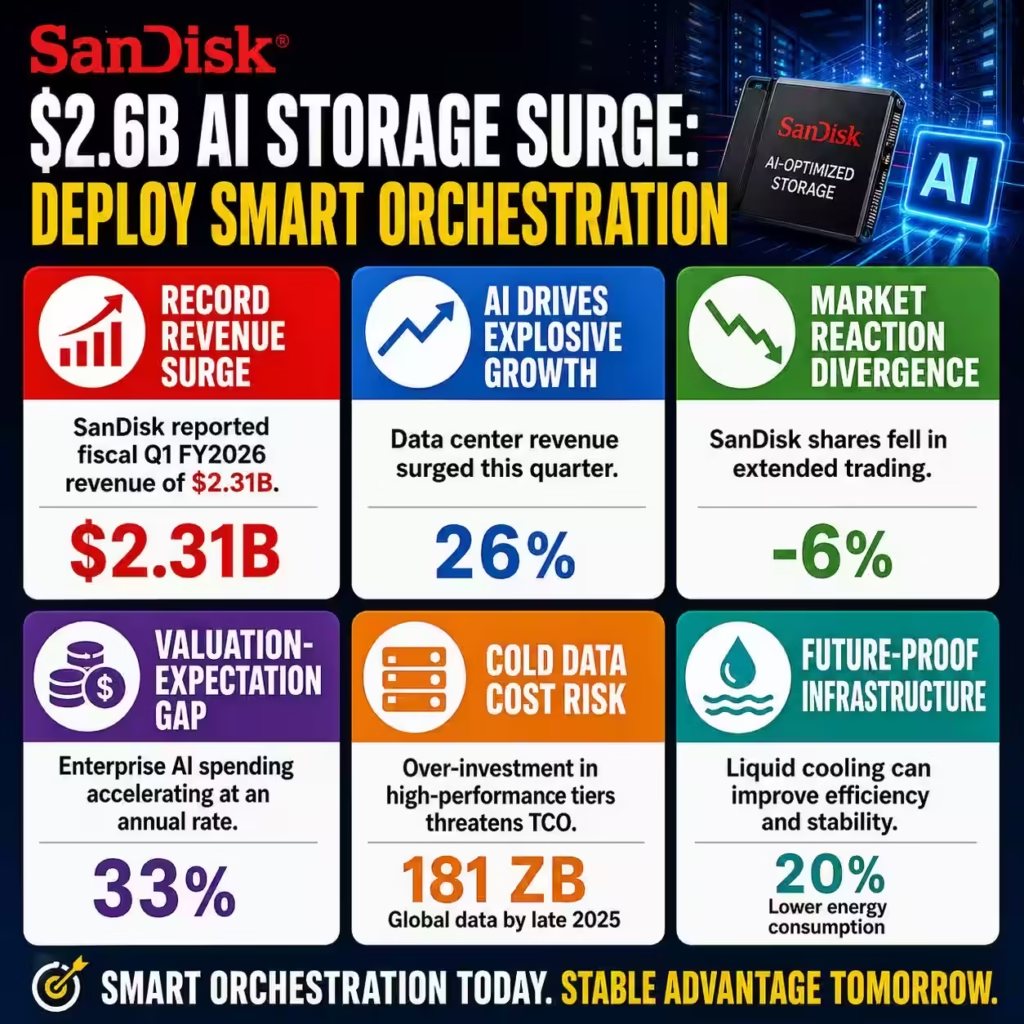

SanDisk reported a fiscal first-quarter 2026 revenue of $2.31 billion, a 21% sequential increase that signals an insatiable enterprise appetite for AI-optimized data storage. This explosive growth follows a trajectory where SanDisk shares rose approximately 350% within a single year, reflecting the market’s aggressive betting on the “HDD Renaissance” and flash storage supremacy. Despite these robust top-line figures, SanDisk shares plummeted over 6% in extended trading, exposing a dangerous disconnect between operational performance and investor sentiment.

The storage sector is currently navigating a period of unprecedented expansion, with global data center investments projected to reach $598 billion by the end of 2025. Data center revenue for SanDisk specifically surged 26% this quarter, driven by the rollout of BiCS8 technology which already accounts for 15% of total bits shipped. Western Digital and Seagate have also forecast quarterly revenues above Wall Street estimates, targeting $3.65 billion and $3.45 billion respectively, as hyperscale capacity remains fully allocated through 2026.

L-Impact Solutions identifies that the primary pain point resides in the “valuation-expectation gap,” where even record-breaking guidance fails to satisfy hyper-inflated market models. Current enterprise AI spending is accelerating at a 33% average annual rate, yet the volatility in SNDK and WDC shares—falling 6% and 8% respectively despite revenue beats—proves financial stability is not guaranteed by demand. To maintain a competitive edge, your organization must look beyond the quarterly numbers and address the structural risks inherent in this AI-driven hardware rush.

L-Impact Solutions: A Strong Critique of the Storage Sector Surge

The recent performance of SanDisk and its peers reveals a systemic risk where short-term stock rallies are detached from the long-term operational sustainability of data center infrastructure. While revenue forecasts are climbing, the 8% drop in Western Digital shares and the 6% slide for SanDisk highlight a fragile market architecture built on speculative enthusiasm. This “AI-driven rally” has masked critical gaps in supply chain resilience and the true cost of scaling high-bandwidth flash (HBF) solutions.

L-Impact Solutions notes that the industry is currently operating on a dangerous “sold-out” model, with production capacity for high-capacity drives committed through 2027. This lack of elasticity means that any geopolitical disruption or manufacturing bottleneck could trigger a catastrophic failure in the AI deployment pipeline. Furthermore, the reliance on high-bandwidth memory (HBM) and specialized AI accelerators has created a hardware monoculture that ignores the rising total cost of ownership (TCO).

The current market logic fails to account for the impending “cold data” crisis, where enterprises are over-investing in expensive performance tiers for workloads requiring economical archival. We observe that while GAAP gross margins for SanDisk have reached 29.8% with an outlook for 42% in Q2, this profitability is highly dependent on five major hyperscale customers. Relying on such a concentrated revenue base creates a binary risk profile for the entire storage sub-sector that could collapse if a single titan pivots.

| Related Analysis: DARPA $54.6B Deep Research: Undersea Drone Growth Plan POET 47% Crash: Governance Fix for Stable Growth Robinhood Stocks 7% Plummet: Diversified Growth Map |

Strategic Solutions for Enterprise Data Infrastructure

Enterprises must diversify their hardware portfolios to include a balanced mix of Solid State Drives (SSD) and high-capacity Hard Disk Drives (HDD) to mitigate pricing power imbalances. By utilizing HDDs for the projected 181 zettabytes of global data expected by late 2025, organizations can reduce storage-related capital expenditure by up to 40%. This hybrid approach ensures that performance-critical AI inference remains on flash while less active training sets reside on cost-effective magnetic media.

Implementing AI-powered storage orchestration software is the second critical solution for managing the complexity of high-density compute racks, which now exceed 20kW per unit. These software-defined networking (SDN) tools can automate metadata tagging and resource pooling, improving data retrieval speeds by a factor of 15x. Advanced orchestration allows your business to move beyond static hardware allocation and toward a dynamic infrastructure that optimizes both power usage effectiveness (PUE) and latency.

Finally, organizations should adopt a multi-vendor procurement strategy to break the “fully allocated” cycle that currently empowers a handful of dominant storage manufacturers. By engaging with emerging vendors in the Asia-Pacific region, which is growing at a 29% rate, firms can secure alternative supply lines and leverage competitive pricing. This geographical and vendor diversification is the only viable method to neutralize the significant pricing power currently held by the industry’s largest incumbents.

Future Prevention Steps for Long-Term Data Stability

The first step in future-proofing your data infrastructure is the mandatory adoption of advanced liquid cooling systems to manage the extreme thermal design power (TDP) of AI clusters. Liquid cooling can improve operational stability and lower energy consumption by 20% compared to legacy air-cooled designs. Investing in this infrastructure now prevents the inevitable hardware degradation and thermal throttling that will occur as AI model sizes continue to expand exponentially through 2030.

Establishing a private cloud or on-premise storage tier is essential for reducing dependency on the volatile pricing models of hyperscale providers. While cloud-based segments will grow, 38% of leading technology firms are already shifting toward on-premise deployments to ensure data sovereignty and predictable TCO. This move provides a safety net against the sudden margin compression or capacity shortages that are becoming common in the public cloud ecosystem.

Lastly, your leadership must integrate “Data Life-cycle Management” (DLM) protocols that automatically migrate aging AI datasets to low-cost, energy-efficient archival tiers. By 2035, hourly electricity demand for US data centers is set to triple, making energy efficiency the ultimate competitive metric. Proactive DLM reduces the physical footprint of your data center and ensures that your storage investments are always aligned with the actual utility of the data stored.

L-Impact Solutions’ Key Takeaway

The storage market is currently trapped in a paradox of record demand and punishing volatility that requires a total recalibration of enterprise strategy. SanDisk’s massive revenue beats mean nothing if your organization is unable to secure the hardware required to run its proprietary AI models during the “fully allocated” 2026-2027 cycle. The 350% rally in storage stocks is a signal to act, but the subsequent 8% corrections serve as a 200-basis-point warning to build fundamental resilience.

Operational success in this era will be defined by those who achieve a 25% reduction in TCO through supply chain diversification and 20% energy savings via advanced liquid cooling. Enterprises must aim for a 40% reduction in storage-related CapEx by migrating “cold data” to high-capacity magnetic media before the next margin-compression cycle begins. Success belongs to the strategists who prioritize a rigorous, workload-aware hybrid-storage architecture over the dangerous pursuit of speculative hardware chasing.

FAQs:

Why did SanDisk stock drop 6% despite $2.31B revenue (+21% QoQ)?

Because the market is pricing beyond performance—until the valuation-expectation gap is corrected, even strong revenue beats will continue to trigger sell-offs.

How does a 350% stock rally still lead to volatility in AI storage companies?

A 350% surge reflects speculative overextension, not sustainable fundamentals—without demand normalization, volatility is structurally inevitable.

What is the risk of relying on hyperscale demand growing at 33% annually?

Overdependence on a few hyperscalers creates a binary revenue risk where even one contract shift can destabilize the entire business model.

Why is the $598B data center investment boom not translating into stable returns?

Capital inflow is outpacing infrastructure resilience, creating a fragile ecosystem where supply constraints and cost inefficiencies erode profitability.

How can enterprises reduce 40% storage CapEx amid AI-driven demand spikes?

Only a hybrid SSD-HDD architecture aligned with data lifecycle management can counter inflated flash costs and restore economic efficiency.