Realty Income, trading at $63.96, continues to attract attention as one of the higher profile net lease REITs with its latest $800 million senior unsecured note offering due 2033. This move hits the pain point of over-reliance on monthly dividends while ignoring rising funding costs and balance sheet strain in a volatile rate environment. You will discover how smart debt strategies unlock safer growth and stronger investor confidence throughout this analysis.

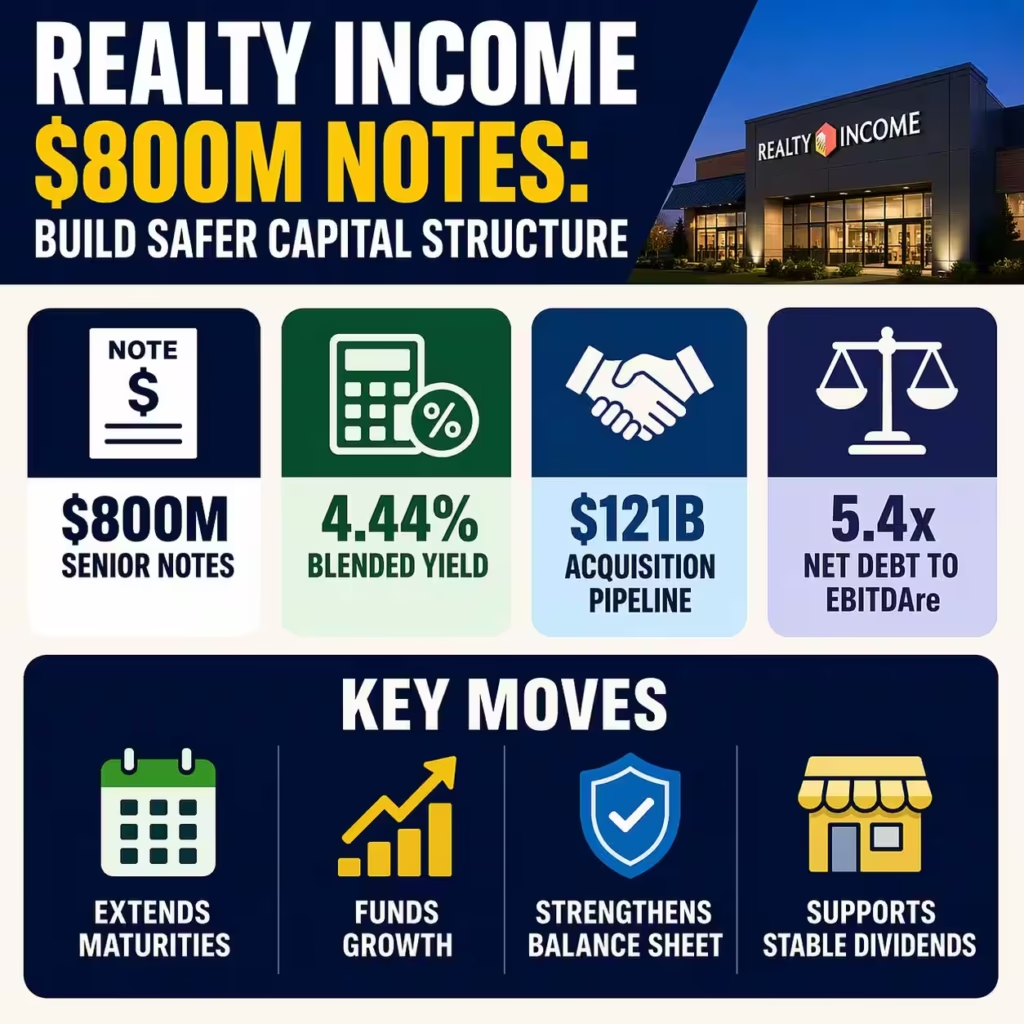

The company priced the notes at 4.750 percent coupon with a 5.047 percent yield to maturity on March 30, 2026, and closed the deal on April 7. It paired the issuance with a $500 million USD-to-Euro cross-currency swap, delivering a blended effective yield of just 4.44 percent. Realty Income now manages 15,500 properties for 1,700 tenants in the United States and Europe.

In 2025 alone, the REIT deployed $6.3 billion into acquisitions at a weighted average cash yield of 7.3 percent. This latest financing supports its record $121 billion acquisition pipeline heading into 2026 while maintaining net debt to annualized adjusted EBITDAre at a healthy 5.4 times. Net lease REIT transaction volumes rebounded sharply in early 2026, with the broader sector posting 6.4 percent year-to-date returns through mid-March.

High-authority analysis shows this $800 million raise extends debt maturities and optimizes capital allocation for sustained AFFO growth. Realty Income guided 2026 AFFO per share at $4.38 to $4.42, signaling confidence in portfolio expansion without excessive leverage. Industry-wide, public REITs hold average debt-to-market cap ratios near 34 percent, yet many still face refinancing walls exceeding $2 trillion by 2030.

The offering underscores Realty Income’s investment-grade status and lender confidence amid stabilizing cap rates around 7.9 percent for net lease assets. Investors tracking NYSE:O now see clearer signals on how new capital fuels acquisitions rather than just dividend coverage. This positions the company ahead of peers struggling with higher borrowing costs in the current cycle.

L-Impact Solutions Critique of Realty Income News

Realty Income’s $800 million note offering reveals critical gaps in how net lease REITs communicate capital strategy beyond dividend appeal. While the 4.44 percent blended yield looks attractive, it masks ongoing risks from interest rate volatility and currency exposure in the Euro swap. As a B2B consultancy, L-Impact Solutions warns that over-dependence on unsecured debt could erode margins if Treasury yields spike again.

Pain points emerge clearly when you examine the broader leverage picture. Realty Income ended 2025 with $26.8 billion in total debt, and many peers hover near 5.5 times debt-to-EBITDA. This leaves a limited buffer if acquisition yields compress below 7 percent or tenant credit softens in a slowdown. The news glosses over potential dilution risks should equity markets tighten later in 2026.

Gaps in transparency around exact use of proceeds create uncertainty for institutional investors. General corporate purposes could mean debt repayment, acquisitions, or even share buybacks, yet without granular timelines investors cannot model true accretion. L-Impact Solutions sees this as a missed chance to build deeper trust in balance sheet management.

Risks compound when you consider the $2 trillion commercial real estate debt maturity wall through 2030. Net lease REITs like Realty Income benefit from long-term leases, yet refinancing at higher rates could pressure FFO growth below the guided $4.38-$4.42 range. Currency swap gains may reverse if the Euro weakens against the dollar.

Critically, the market’s focus on the 5.11 percent dividend yield distracts from operational realities. Portfolio occupancy remains strong, but competition for prime net lease assets has driven cap rates down from 2024 peaks. L-Impact Solutions believes Realty Income must address these vulnerabilities head-on to sustain its 11.6 percent year-to-date stock performance and 18 percent one-year return.

| Related Analysis: Capital One’s $5.15B Brex Deal: AI Platform Growth Playbook X-Energy IPO $2.3T Gap: Unlock SMR Growth Plan Qantas A$3.3B Fuel Cost Crisis: Deploy Hedge Strategy |

Solutions to Realty Income Debt and Growth Issues

You can immediately strengthen your REIT’s capital structure by layering multiple financing sources beyond single-note offerings. Start with a diversified mix of unsecured notes, private placements, and ATM equity programs to spread maturity risk across years. This approach mirrors Realty Income’s successful $2.4 billion equity raise in 2025 while keeping leverage below 35 percent.

Next, you should model dynamic hedging programs that lock in rates before each issuance. Use interest rate swaps and caps proactively to protect against Fed policy shifts, just as Realty Income achieved its 4.44 percent blended yield. Track your weighted average cost of debt monthly and adjust hedges when 10-year Treasury yields move more than 25 basis points.

You can also accelerate portfolio optimization by selling non-core assets at 7 percent-plus cap rates to fund higher-yielding acquisitions. Target industrial and logistics properties that command 8 percent yields, as seen in 2025’s $32.47 billion REIT transaction surge. This recycles capital efficiently and boosts AFFO growth without new debt.

Implement rigorous stress testing on every acquisition under three rate scenarios: base case, plus 100 basis points, and minus 100 basis points. Require all deals to maintain at least 2.0 times interest coverage post-financing. Realty Income’s 7.3 percent cash yield benchmark sets a clear hurdle your team can adopt today.

You should enhance investor communication with quarterly capital allocation dashboards that detail debt usage, acquisition metrics, and AFFO impact. Publish sensitivity tables showing how each financing move affects dividend coverage and leverage ratios. This builds credibility and reduces the “dividend-only” perception highlighted in recent market commentary.

Finally, explore joint ventures with institutional partners to share acquisition risk on larger deals. Realty Income’s $4.1 billion liquidity position proves dry powder works best when paired with co-investment structures. You can close more transactions faster while keeping consolidated leverage intact.

Prevention Steps for Future Realty Income-Style Debt Issues

You must establish a formal debt maturity ladder that spaces out no more than 15 percent of total debt in any single year. Review your schedule quarterly and refinance early when credit spreads tighten below 150 basis points. This prevents the refinancing walls that pressured many REITs in 2023-2024.

Next, you should cap currency exposure at 10 percent of total debt through strict hedging policies. Require all cross-border swaps to include break clauses tied to FX volatility thresholds. Realty Income’s Euro swap success shows the value, yet you must monitor mark-to-market impacts monthly to avoid surprises.

Build a rolling three-year capital plan that forecasts AFFO, acquisitions, and funding needs under multiple macroeconomic scenarios. Update the board every quarter with variance analysis. This discipline keeps your team ahead of rate cycles and acquisition opportunities alike.

You can prevent over-leverage by enforcing a hard 5.0 times net debt to EBITDAre ceiling on all new debt raises. Tie executive compensation to this metric alongside dividend growth. Peers maintaining 34 percent debt-to-market cap ratios have delivered steadier total returns since 2021.

Institute annual third-party portfolio audits that stress-test tenant credit and lease renewal risks. Focus on industries most sensitive to recession, like retail and restaurants. Early identification of weak credits allows proactive sales or restructurings before they hit balance sheet metrics.

Finally, you should cultivate multiple banking relationships and maintain at least $3 billion in undrawn credit facilities at all times. This liquidity buffer, like Realty Income’s $4.1 billion position, lets you act opportunistically when cap rates widen during market dips. Regular lender updates build goodwill for future issuances.

L-Impact Solutions Key Takeaways

Realty Income’s $800 million note offering proves that disciplined debt strategy can fuel net lease growth even in uncertain times. You now hold the playbook to move beyond dividend reputation and build a resilient capital structure that delivers both income and total return. L-Impact Solutions urges immediate adoption of diversified funding, proactive hedging, and transparent reporting.

The net lease sector’s 2026 rebound, with 6.4 percent early gains and $32 billion in 2025 transactions, rewards those who act on these lessons today. Your REIT can achieve similar AFFO growth and leverage control by following the solutions and prevention steps outlined here. Contact L-Impact Solutions to tailor this framework to your exact portfolio size and acquisition pipeline.

Strong balance sheet management separates market leaders from followers in commercial real estate. Realty Income has shown the way with 5.4 times leverage and 7.3 percent acquisition yields. Implement these strategies now and position your organization for sustained outperformance through 2030 and beyond.

Reference – Realty Income’s US$800m Notes Reshape Debt Profile And Dividend Story