Learn POET’s 47% drop and discover governance strategies that support resilience, trust, and stable future growth.

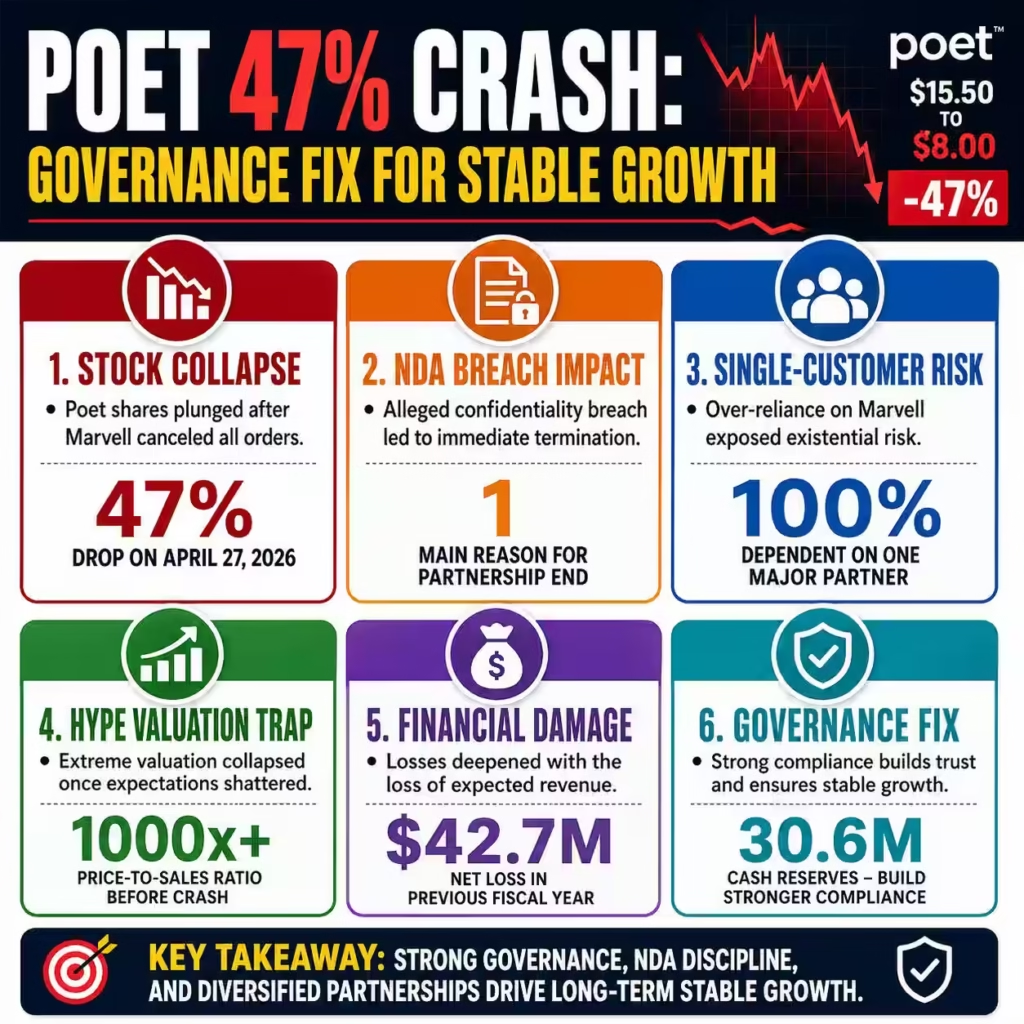

Poet Technologies’ stock plummeted 47% on April 27, 2026, after Marvell Technology abruptly terminated all purchase orders following alleged breaches of confidentiality. This record-breaking liquidation reflects a broader systemic fragility in the semiconductor sector where high-stakes confidentiality breaches can instantly evaporate billions in theoretical market valuation. The central pain point lies in the volatile intersection of aggressive retail speculation and the rigid legal frameworks governing tier-one hardware integrations.

This analysis explores the strategic missteps leading to this $15.50-to-$8.00 freefall and provides the necessary B2B frameworks to insulate your enterprise from similar partnership dissolutions. Real-world data indicates that the AI optical transceiver market is projected to hit $26 billion by late 2026, making these infrastructure failures particularly costly for scaling firms. High-authority analysis reveals that Poet’s failure was not merely technical but a fundamental breakdown in corporate governance and non-disclosure agreement (NDA) management.

The fallout began when Marvell, holding a market capitalization of approximately $143.68 billion, issued a written notice on April 23, 2026, to cancel all orders with Poet. Investors, who had pushed Poet’s stock to a multiyear high of $15.50 just days prior, were blindsided by the disclosure of this termination on the following Monday. This delay in reporting, where management allegedly held the news over a weekend while the stock rallied 29%, has triggered intense scrutiny.

The technical core of the partnership involved Poet’s Optical Interposer™ technology, designed to facilitate high-speed data transfer in AI data centers. Current market trends show that North American hyperscale data centers are sustaining over 30% annual growth, requiring reliable interconnect solutions. However, when a supplier fails to maintain the sanctity of a tier-one relationship, the technical merits of the hardware become secondary to the legal and reputational risks.

Poet’s CFO had previously confirmed the Marvell relationship in public interviews, a move that Marvell later cited as a breach of confidentiality obligations. This event highlights a massive disconnect between the “pump and dump” nature of retail-driven AI stocks and the conservative operational requirements of semiconductor giants. Marvell’s decision to walk away suggests that for major players, protecting intellectual property and trade secrets is more valuable than any single component supplier.

Data from 2025 shows that the NLP chipset segment reached $18.8 billion, driven by massive demand for low-latency inference hardware. Poet was positioned to capture a significant share of this, yet they lost their primary gateway into the Nvidia-Marvell ecosystem. The market reaction—a 50% haircut in a single session—serves as a grim reminder of the “single-customer risk” that plagues small-cap tech firms.

Analysts note that Poet’s valuation, which recently sat at a price-to-sales ratio exceeding 1000x, was built on expectations of a seamless ramp-up. When that ramp-up hit a legal wall, the speculative floor fell through entirely. Furthermore, the timing of Marvell’s cancellation coincided with its strategic acquisition of other technology players like Polariton and Celestial AI.

These acquisitions provided Marvell with alternative pathways to high-speed photonics, potentially making Poet’s technology redundant or less critical. In the B2B semiconductor space, the “design-in” phase is often protected by ironclad NDAs that prevent even the mention of a partner’s name. By violating these norms, Poet management committed a cardinal sin of the industry: prioritizing short-term stock price momentum over long-term contractual stability.

The resulting $42.7 million net loss reported in the previous fiscal year now looks even more daunting without the projected Marvell revenue. As AI infrastructure scales, the demand for 800G and 1.6T transceivers will only intensify, yet Poet now finds itself on the outside looking in. This case study proves that in the race for AI dominance, silence is often as valuable as silicon.

L-Impact Solutions Critique: The Systemic Failure of Governance and Compliance

L-Impact Solutions views the Poet Technologies situation as a textbook example of a “governance-induced disaster” that could have been mitigated through rigorous compliance protocols. The primary pain point here is not the technology, which remains theoretically sound, but the amateurish handling of material non-public information (MNPI). Marvell’s cited reason for cancellation—the disclosure of purchase order and shipping information—indicates a complete lack of internal communication controls within Poet’s C-suite.

We identify three major risks: the transparency gap, the single-node dependency, and the “hype-cycle” valuation trap. When a company’s valuation is 100% dependent on a single partnership, any friction in that relationship is an existential threat. Poet’s management chose to engage with retail influencers and YouTube analysts, a strategy that often backfires when dealing with institutional partners who value discretion.

The risks associated with “talking up” a contract before it reaches the mass-production stage cannot be overstated. In the high-stakes world of AI networking, where Marvell competes with giants like Broadcom (holding 70% market share), secrecy is a competitive weapon. By leaking details, Poet essentially compromised Marvell’s strategic roadmap, forcing a swift and punitive termination to protect their broader ecosystem.

L-Impact Solutions notes a significant gap between Poet’s “strategic priorities” and their tactical execution of legal duties. A company with a $30.6 million derivative warrant liability and a $11.6 million negative operating cash flow cannot afford to alienate its largest source of potential revenue. The governance failure is further highlighted by the fact that the cancellation was known on a Thursday but not disclosed until the following Monday.

This suggests a lack of fiduciary responsibility to shareholders and opens the door for significant class-action litigation. Furthermore, the “hype-cycle” trap is evident in how the stock was promoted. Paying influencers to drive retail sentiment while a short-seller report from Wolfpack Research was already circling created a “tinderbox” environment.

When the Marvell news broke, it didn’t just cause a dip; it caused a total collapse because there were no institutional “diamond hands” to hold the floor. Our analysis suggests that Poet’s move to redomicile to the United States was a reactive attempt to solve tax issues, rather than a proactive move to improve governance. The gap in this business model is the failure to diversify.

Relying on a single $5 million order as a “fallback” when a multi-billion dollar partnership evaporates is not a strategy; it is a desperate pivot. Companies must realize that in the B2B tech sector, your reputation for reliability is the only currency that matters in the long run. The collapse proves that without rigid internal protocols, even the best technology will fail to reach the commercial market.

| Related Analysis: Intel 20% Surge: Does it Hide $2.5B Foundry Loss? Delta A350-1000 Expert Analysis: Smart Cash Flow Plan Buffett’s 226% Warning Research Article: Risk Exit Plan |

Comprehensive Solutions: Restructuring Partnerships for AI Resilience

To resolve the issues identified in the Poet-Marvell fallout, enterprises must implement a “Triple-Lock” partnership framework. First, you must establish an Independent Compliance Office (ICO) that vets every public statement made by executives, including social media and “casual” interviews. This office should have the power to veto any communication that references specific customer names or order volumes without written consent from the partner.

Second, you must aggressively pursue “Customer Diversification Parity” (CDP), ensuring that no single client accounts for more than 25% of projected revenue. Poet’s over-reliance on the Marvell/Celestial AI pipeline was their undoing; a diversified portfolio would have cushioned the 50% blow. Third, utilize Escrow-Based IP Protection, where sensitive shipping and production data are stored in secure, third-party environments that only release information to stakeholders on a strictly need-to-know basis.

Furthermore, firms should shift from “Announcement-Driven” to “Milestone-Driven” investor relations. Instead of celebrating the signing of a purchase order—which can be canceled—celebrate the successful completion of a product’s lifecycle or the attainment of a specific revenue threshold. This reduces the volatility associated with “news” and builds long-term investor confidence based on actual performance.

For companies in the optical interconnect space, where the market is expected to reach $50 billion by 2032, technical excellence must be paired with operational maturity. You should also implement “Automated Disclosure Triggers” (ADT) within your legal tech stack. These systems ensure that if a material contract is terminated, the disclosure is drafted and filed with the SEC/NASDAQ within hours, not days, preventing the “weekend delay” scandal.

Another critical solution is the adoption of “Relationship Insurance” through multi-tier agreements. Instead of one monolithic contract, break the partnership into smaller, task-specific Work Orders. This way, a breach in one area (like a minor shipping leak) does not necessarily terminate the entire relationship.

It allows for “partial failures” where the partnership can be salvaged through fines or corrective actions rather than a total scorched-earth cancellation. Finally, we recommend that tech companies engage in “Red-Teaming” their own governance. Hire external consultants to attempt to leak information or find gaps in your NDAs before a partner like Marvell does.

By finding your own weaknesses, you prevent them from being used against you in a contract termination. These solutions provide a roadmap for small-cap semiconductor firms seeking to scale without losing control. Implementing these changes will create a more stable environment for technical and financial growth.

Prevention Methods: Insulation Against Future Supply Chain and Legal Volatility

Prevention begins with the “Executive Media Gag-Rule” for any company currently in the design-in phase with a tier-one semiconductor firm. You must train your C-suite to understand that “confirming” a rumor is just as damaging as leaking a secret. Prevention also requires a “Strategic Buffer Fund” equal to twelve months of operating expenses, ensuring that even if a major contract is lost, the company does not face immediate insolvency.

Poet’s negative cash flow meant they were living “paycheck to paycheck” on the hope of Marvell orders; this is a high-risk gamble that should be avoided. Use predictive analytics to monitor “Partner Sentiment” by analyzing their acquisitions and public filings. If your partner acquires a direct competitor to your technology, you should already be executing your “Plan B” diversification strategy.

On the legal front, you must include “Cure Periods” in your NDAs. A cure period allows a company a set amount of time to rectify a breach before the contract can be terminated. While Marvell was within its rights, a more robustly negotiated contract might have allowed Poet to survive the breach.

Additionally, you must implement “Internal Information Siloing” (IIS). This ensures that the engineering team working on the product does not have access to the financial details of the purchase order. By compartmentalizing data, you minimize the chance that a single employee can inadvertently leak enough information to trigger a contract violation.

Future-proofing also involves moving away from “Influencer-Based” marketing in the B2B sector. While it may drive short-term retail interest, it creates a “transparency debt” where the company feels pressured to provide “alpha” to its followers. Instead, focus on “Institutional Credibility” by attending industry-standard conferences and presenting peer-reviewed technical papers.

Data shows that firms with higher institutional ownership experience 30% less volatility during contract disputes. Finally, ensure your “Disaster Recovery Plan” includes a pre-drafted “Pivot Strategy.” If a major partner leaves, you should have a list of three “Plan B” customers ready for immediate engagement.

This allows you to issue a press release that shows momentum despite a specific loss. Such a strategy would have likely prevented Poet’s total market crash. Prevention is always cheaper than rebuilding a collapsed reputation.

L-Impact Solutions Key Takeaway: The Hard Truth of the AI Hardware Race

L-Impact Solutions asserts that the Poet Technologies collapse is a mandatory wake-up call for every B2B tech executive. You cannot run a billion-dollar semiconductor play like a small-town startup. If you prioritize “stock pump” optics over “contractual integrity,” the market will eventually find your true value, and it will be painful.

The 50% drop is not a “market overreaction”; it is a market correction for a company that proved it cannot handle the responsibilities of a tier-one partner. In the AI sector, where speed is everything, Marvell’s ruthless termination is the new standard of business. They have no time for partners who cannot keep a secret.

To stay competitive, you must professionalize your investor relations and legal compliance immediately. The AI optical market is growing at a 57% YoY rate, and the opportunities are vast, but they are reserved for the “adults in the room.” If your CFO is spending more time on YouTube than in legal review, you are already at risk.

We recommend a complete audit of all active NDAs and a restructuring of how you disclose “wins” to the public. Remember: in the semiconductor world, a signed purchase order is a liability until the product is shipped, paid for, and the NDA expires. Protect your silence to protect your stock price.

FAQs:

Why did Poet Technologies stock crash 47% from $15.50 to $8.00 in one day after the Marvell fallout?

The collapse shows that when valuations depend more on hype than diversified revenue, one governance mistake can erase shareholder trust overnight.

How can semiconductor firms avoid a 50% market wipeout caused by confidentiality breaches?

Companies need stricter NDA enforcement, executive media controls, and board-level compliance oversight because weak communication discipline is an expensive avoidable risk.

Why is single-customer dependency dangerous when one lost deal can destroy billions in market value?

Relying heavily on one strategic buyer is poor risk architecture, and resilient firms should cap customer concentration well below existential levels.

What does a 1000x price-to-sales valuation say about speculative AI hardware stocks?

Extreme multiples often signal unrealistic expectations, and management should prioritize execution milestones over feeding momentum-driven narratives.

How can AI optical transceiver firms win in a $26 billion 2026 market without repeating Poet’s mistakes?

The winners will combine strong photonics innovation with mature governance, diversified contracts, and disciplined investor relations instead of shortcut publicity tactics.