Intel rises 20% on turnaround momentum, signaling strategic progress while balancing execution risks and long-term growth potential.

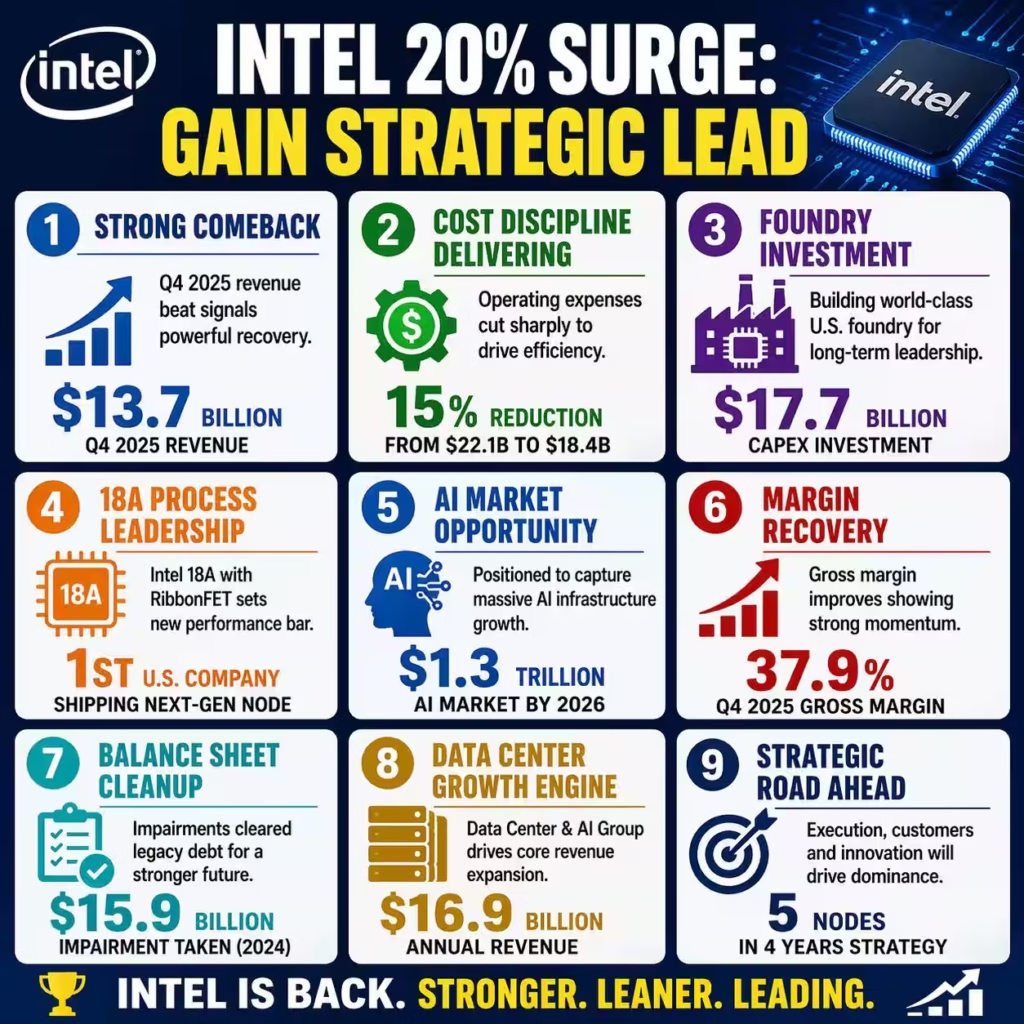

Intel’s stock soared 20% as fourth-quarter 2025 revenue reached $13.7 billion, surpassing analyst estimates and signaling a pivotal recovery for the legacy chipmaker. This explosive growth follows a catastrophic fiscal year 2024 where the company recorded a staggering $18.8 billion net loss. The primary pain point remains the massive capital intensity required to transition from a pure-play designer to a world-class merchant foundry. This article explores how aggressive cost-cutting measures and the technical maturation of the 18A process node provide a roadmap for your enterprise to stabilize volatile margins.

Recent data indicates that Intel has already reduced its operating expenses by 15%, dropping from $22.1 billion to $18.4 billion within a single fiscal cycle. Such a drastic reduction in overhead demonstrates a commitment to lean operations that every B2B leader must study. High-authority analysis suggests that Intel’s survival hinges on its ability to capture a portion of the $1.3 trillion AI infrastructure market by 2026.

While the current 6% global market share is a shadow of its 2021 peak, the underlying momentum is undeniable. You can observe a clear shift in sentiment as institutional investors begin to price in the successful execution of the “five nodes in four years” strategy. The narrow net loss of only $267 million in 2025 marks the beginning of a new era of fiscal responsibility.

Effective resource allocation is the hallmark of this turnaround, as the company moved from a position of terminal decline to one of calculated expansion. You must recognize that the $15.9 billion in impairment charges taken in late 2024 were necessary to clear the balance sheet of legacy technical debt. This strategic “cleansing” allowed for a cleaner gross margin recovery, which reached 37.9% in the most recent quarter.

The adoption of the Intel 18A process, featuring GAA RibbonFET transistors, positions the firm as the only U.S.-based manufacturer shipping next-generation logic at scale. Such technical leadership is critical when competing against titans like TSMC and Samsung for external foundry contracts. Industry reports show that custom ASIC shipments from hyperscalers are projected to grow by 44.6% in 2026, offering a massive tailwind.

By focusing on the high-growth segments of AI PCs and data center accelerators, the organization is effectively retooling its entire value proposition. Your business can learn from this focus on core competencies while shedding underperforming assets to maintain liquidity. The deconsolidation of Altera and the partial monetization of Mobileye provided the necessary cash infusion to fund $17.7 billion in capital investments. Strategic agility is no longer optional in a market where Nvidia controls over 32% of the AI chipset revenue.

L-Impact Solutions Critique: The Hidden Fragility of the Intel Pivot

L-Impact Solutions views the recent 20% stock surge as a temporary relief rally that masks deep structural risks within the Intel Foundry business model. While the revenue beat is encouraging, the foundry segment continues to hemorrhage cash, posting an operating loss of $2.5 billion in the fourth quarter of 2025 alone. We identify a significant gap between the company’s technical milestones and its actual ability to attract tier-one external customers at high volumes.

The reliance on internal wafer sourcing for nearly 90% of current foundry output creates a dangerous echo chamber for margin reporting. Without a major anchor tenant like Apple or Qualcomm, the $100 billion total addressable market for merchant foundries remains largely out of reach. We observe that the 15% workforce reduction, while fiscally prudent, has led to a critical loss of senior engineering talent to competitors.

This brain drain could jeopardize the long-term reliability of the 14A process roadmap scheduled for late 2026. Furthermore, the debt-to-equity ratio remains a concern as total liabilities stand at a formidable $85.07 billion despite recent repayments. The “shell-ahead” strategy, which involves building out massive fabrication facilities before securing orders, is an incredibly high-risk gamble.

The market’s current valuation of Intel at over 120 times forward earnings suggests an optimism that may not be supported by mid-term cash flow projections. L-Impact Solutions notes that the $500 million revenue miss for the Gaudi 3 AI accelerator highlights a persistent software ecosystem gap. While the hardware is competitive on a price-to-performance basis, the lack of CUDA-equivalent library maturity limits enterprise adoption.

This represents a fundamental risk to the Data Center and AI Group, which currently generates $16.9 billion in annual revenue. Competitive pressure from AMD’s EPYC processors continues to erode Intel’s data center market share, which has dropped significantly over the last three years. We also find the heavy reliance on U.S. government subsidies through the CHIPS Act to be a double-edged sword that invites regulatory scrutiny. If federal milestones for the $8.5 billion grant are not met with surgical precision, the company faces a liquidity crunch.

The current 34.8% gross margin is still well below the 60% industry standard required for sustainable R&D leadership. Businesses must be cautious of following this “aggressive expansion” model without first securing a diversified and committed customer base. The volatility of the semiconductor cycle means that any delay in the 18A ramp could lead to another round of massive asset impairments.

| Related Analysis: USA $4B Value Rare Earth: Strengthen Supply Chains AAPL $4T Q2 2026: Capture Emerging Market Growth Avis 86.2% Short Crisis: Protect Your Capital |

Strategic Solutions: Reclaiming Dominance Through Diversified Revenue Streams

To mitigate the risks identified, Intel must prioritize the expansion of its external foundry customer base beyond small-scale government projects. We recommend a “Land and Expand” strategy where the company offers highly subsidized initial runs on the 18A node to major hyperscalers like Amazon and Google. By capturing even 4% of the external foundry market, the organization could generate an additional $4 billion in annual high-margin revenue.

This transition requires a fundamental shift in corporate culture from an internal-first mindset to a service-oriented foundry model. You should implement a dedicated “Foundry Success” division that mimics the high-touch customer service found in software-as-a-service industries. The second solution involves aggressively developing an open-source AI software stack to rival Nvidia’s proprietary ecosystem.

Investing $2 billion into the OneAPI initiative will lower the barrier to entry for developers who are currently locked into the CUDA environment. Market data suggests that enterprise users are desperate for a viable alternative to reduce their total cost of ownership. Providing seamless software compatibility will accelerate the adoption of Gaudi accelerators and Xeon processors in diverse workloads.

Furthermore, Intel must optimize its capital expenditure by utilizing “Smart Capital” partnerships similar to the $11 billion Apollo joint venture. This allows the company to build necessary infrastructure while keeping significant debt off the primary balance sheet. Such financial engineering is essential when the goal is to maintain a cash reserve of at least $37 billion for unforeseen market shifts.

You can adopt this strategy by seeking co-investment partners for your own high-cost infrastructure projects to distribute risk. The company should also double down on the “AI PC” category, where it already holds a dominant position in the laptop market. By integrating NPU technology into every Core Ultra processor, Intel creates a standardized platform for the next generation of local AI applications.

Current projections estimate that 60% of all PCs shipped by 2027 will be AI-capable, representing a massive volume play. This hardware-software synergy will protect the Client Computing Group’s $32.2 billion revenue base from ARM-based competitors. Finally, a renewed focus on the “Edge” market through the Network and Edge Group can capture the growing demand for real-time AI inferencing. Edge computing revenue is expected to grow at a CAGR of 15% through 2030, offering a stable and high-margin niche.

Prevention Methods: Future-Proofing Against Market Volatility and Technical Stagnation

Preventing future financial crises requires a rigorous “Technical Audit” protocol that ensures roadmap milestones are based on realistic yield data rather than marketing targets. Intel must implement a “Red Team” approach to its R&D process, where internal units are incentivized to find flaws in upcoming process nodes. This will prevent the type of multi-year delays that plagued the 10nm and 7nm transitions, which cost the company billions in lost market share.

Organizations can implement similar internal audits to ensure product launches are backed by verified performance metrics. A second prevention step involves the creation of a “Talent Retention Fund” specifically for world-class lithography and chip design experts. By offering equity-based incentives tied to long-term technical milestones, the company can stabilize its intellectual capital.

Losing key engineers during a critical transition is often the primary reason for architectural failures in the semiconductor industry. Data shows that companies with stable leadership teams in engineering roles outperform their peers by 22% in product cycle efficiency.

Supply chain resilience must also be prioritized to avoid the inventory drawdowns that impacted the Client Computing Group in early 2024. Intel should diversify its raw material sourcing and increase its “buffer stock” of critical chemicals and gases required for EUV lithography. Developing a localized supply chain within North America and Europe will mitigate the risks associated with geopolitical instability in the Pacific.

You should analyze your own supply chain for single points of failure and establish redundant vendors for your most critical components. Another vital prevention method is the implementation of a “Variable Cost Structure” that allows the company to scale operations up or down based on quarterly demand. By utilizing a mix of permanent and contract labor in non-core functions, the organization can protect its margins during cyclical downturns.

This flexibility would have saved approximately $1.2 billion during the 2023 market contraction. Finally, maintaining a transparent and frequent communication channel with institutional investors is essential to prevent extreme stock price volatility. Providing granular data on foundry yields and external customer win-rates will build long-term trust and lower the cost of capital. Consistency in meeting guidance is the most powerful tool for stabilizing a company’s market valuation.

L-Impact Solutions Key Takeaway: The Verdict on Intel’s Resurrection

The 20% surge in Intel’s stock is a testament to the power of radical transparency and aggressive restructuring in the face of an existential crisis. L-Impact Solutions asserts that while the company has successfully “stopped the bleed,” it has not yet won the war for semiconductor supremacy. The success of the next three fiscal years depends entirely on the impeccable execution of the 18A process and the acquisition of non-Intel customers.

We believe that the $18.5 billion swing in the bottom line from 2024 to 2025 proves that big-tech turnarounds are possible through disciplined capex. However, you must remain vigilant, as the foundry operating losses are currently being subsidized by the legacy PC business. This “internal subsidy” model is only sustainable if the PC market remains robust and the AI PC transition gains rapid consumer traction.

Our opinion is that Intel is a “Strong Hold” for enterprises looking to diversify their hardware partnerships away from the Nvidia-TSMC monopoly. The strategic importance of a U.S.-based leading-edge foundry cannot be overstated in the current geopolitical climate. We recommend that you monitor the Q1 2026 earnings for a confirmed external customer name as the ultimate signal of foundry viability.

Intel’s journey from a $16.6 billion quarterly loss to a near-breakeven state is one of the most significant events in modern business history. Every B2B leader should view this as a case study in managing massive technical debt while pursuing high-growth innovation.

FAQs:

How can Intel sustain its 20% stock surge when Intel Foundry still lost $2.5 billion in Q4 2025?

The rally looks encouraging, but Intel must urgently convert foundry momentum into profitable external contracts or investor optimism could fade quickly.

Why is Intel’s $85.07 billion liability load a major risk despite revenue reaching $13.7 billion in Q4 2025?

Strong quarterly revenue helps sentiment, yet such heavy liabilities can restrict future innovation spending and pressure long-term competitiveness.

Can Intel’s 18A process node realistically challenge TSMC and Samsung with only 6% global market share left?

The technology is promising, but execution speed and winning marquee customers matter far more than roadmap announcements alone.

Will Intel’s 15% operating expense cut from $22.1B to $18.4B damage engineering talent and future growth?

Cost discipline is necessary, but aggressive cuts that weaken top technical talent could create bigger strategic losses later.

How important is the $1.3 trillion AI infrastructure market to Intel’s turnaround by 2026?

It is critical, because without capturing meaningful AI accelerator and data center share, Intel’s recovery may remain incomplete.

Reference – Intel’s stock soars 20% as results top estimates, with chipmaker showing signs of growth