AMD’s $10.25B surge exposes critical AI supply risks; secure your capacity, control your costs, and protect your scale now.

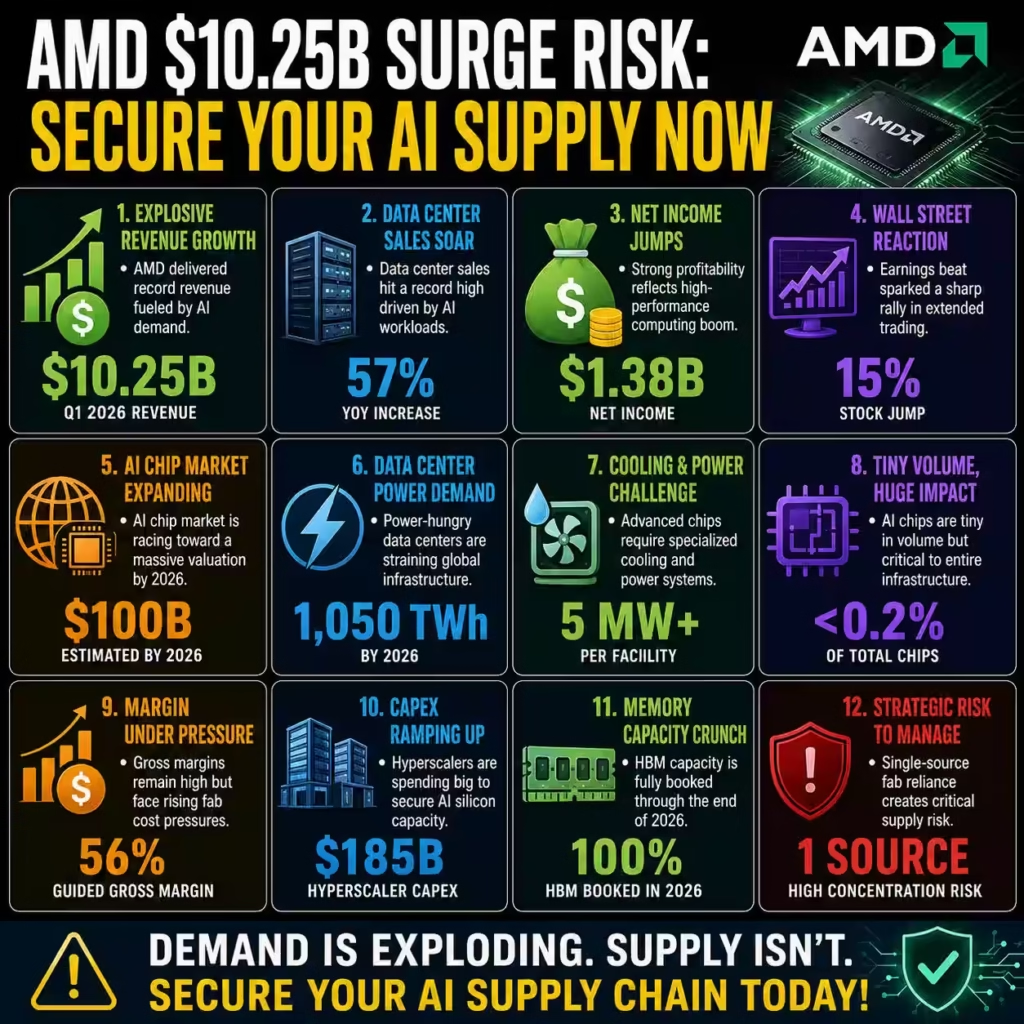

Advanced Micro Devices (AMD) reported an explosive first-quarter 2026 revenue of $10.25 billion alongside an adjusted EPS of $1.37, crushing conservative expectations as enterprise demand for artificial intelligence workloads escalates globally. This massive 38% year-over-year revenue surge exposes a critical industry pain point regarding global semiconductor supply chain capacity limits that threaten enterprise scaling timelines. You can overcome these severe infrastructure bottlenecks by implementing the strategic sourcing and operational resilience methods outlined in this comprehensive business analysis.

Data center sales specifically increased by an unprecedented 57% to $5.8 billion compared to $3.67 billion in the same period last year. This rapid growth directly reflects the broader artificial intelligence chip market rapidly expanding toward an estimated $100 billion valuation by the end of 2026. Enterprise leaders must acknowledge that capturing this infrastructure growth requires immediate navigation of the structural supply chain bottlenecks currently dominating global semiconductor production.

Net income rose substantially to $1.38 billion, representing 84 cents per share, up from $709 million during the previous year. Advanced Micro Devices is clearly monetizing the transition to high-performance computing, but sustaining this momentum demands securing limited foundry capacity from top-tier silicon fabrication partners. Industry data confirms that generative artificial intelligence chips now represent the primary margin driver for semiconductor firms globally despite their low production volume.

Global data center electricity consumption is projected to reach an astounding 1,050 terawatt-hours by 2026, placing massive strain on existing power infrastructure. Advanced processors require specialized high-density cooling and power delivery systems that traditional legacy colocation facilities simply cannot support today. Market participants must rethink their facility deployments because acute energy constraints will dictate operational success more than pure silicon hardware availability.

Wall Street reacted aggressively to the earnings beat, pushing the stock up approximately 15% in extended trading sessions. However, this valuation multiple compression indicates investors are pricing in flawless execution despite documented, severe shortages in high-bandwidth memory supplies. Your firm must recognize that market exuberance often masks the underlying fragility of the specialized analog and enterprise computing component supply chains.

The global semiconductor sector will reach roughly $975 billion in total sales in 2026, largely driven by this specific artificial intelligence infrastructure boom. Despite this massive top-line industry figure, artificial intelligence accelerators represent less than 0.2% of total global chip production volume. This extreme concentration creates isolated vulnerabilities where a single component shortage can delay entire enterprise networking mega-cluster deployments for several months.

Advanced Micro Devices guided non-GAAP gross margins to roughly 56% for upcoming quarters, indicating tight pricing power amid rising fabrication costs. Maintaining these premium margins will require ruthless supply chain efficiency and prioritized capacity allocations from overseas manufacturing partners. Business leaders should observe this margin compression pressure as a leading indicator of rising hardware acquisition costs across the enterprise computing landscape.

Total artificial intelligence data center power capacity reached 30 gigawatts recently, effectively matching the peak power usage of major geographic regions like New York State. Supporting AMD hardware at scale means competing directly for commercial real estate equipped with massive five-megawatt and higher power allocations. The successful deployment of high-performance computing clusters now requires parallel, heavy capital investments in advanced liquid cooling and distributed energy resources.

Hyperscale technology companies are allocating roughly $185 billion in capital expenditures this year alone to secure these high-performance silicon assets. This extreme capital concentration leaves middle-market enterprise buyers fighting over limited remaining allocations of critical networking and compute hardware. Corporate technology officers must pivot away from transactional purchasing toward long-term strategic vendor partnerships to guarantee critical server hardware availability.

Current semiconductor inventory dynamics reveal that major memory producers have already fully booked their high-bandwidth memory capacity through the end of 2026. Because advanced graphics processing units cannot function without these specific memory stacks, final product lead times will extend significantly across all vendors. Procurement teams must adapt their capacity forecasting models to accommodate these structural delays or risk stalling major corporate digital transformation initiatives.

Critique Opinion on Advanced Micro Devices Performance

L-Impact Solutions views the recent AMD financial performance as an impressive commercial victory that simultaneously exposes deep vulnerabilities across the global technology stack. While the $10.25 billion revenue figure commands attention, it masks the severe concentration risk inherent in relying on single-source offshore fabrication for advanced nodes. Enterprise buyers celebrating these silicon advancements must immediately audit their downstream dependencies to avoid being caught in impending hardware allocation bottlenecks.

The reported 57% surge in data center revenue highlights a dangerous industry pivot where vendors prioritize premium artificial intelligence products at the expense of standard enterprise hardware. We strongly critique the lack of transparency regarding how this explosive top-line growth impacts the availability of traditional central processing units and mature semiconductor nodes. Your business operations likely rely heavily on these neglected legacy components that face increasing supply constraints as fabrication lines pivot to high-margin accelerators.

Advanced Micro Devices currently navigates a fragile supply chain where the availability of high-bandwidth memory strictly caps its ability to manufacture finalized graphic processing units. We assess this external dependency as a critical systemic gap, because even flawless internal engineering cannot overcome external supplier deficits in specialized memory packaging. Corporate procurement directors must realize that purchasing an advanced server today requires navigating the delayed lead times of dozens of constrained sub-components.

The jump in net income to $1.38 billion is financially robust but obscures the massive research and capital expenditure required to maintain parity in the semiconductor arms race. L-Impact Solutions warns that this severe capital intensity forces vendors to lock enterprise clients into restrictive, long-term hardware ecosystems to guarantee their own return on investment. You must aggressively defend your infrastructure agility by avoiding proprietary software stacks that eliminate your ability to switch hardware providers.

Wall Street’s 15% stock price jump reflects a dangerous market assumption that physical manufacturing capacity can scale infinitely alongside software demand. We argue that global fabrication facilities are approaching hard physical limits regarding extreme ultraviolet lithography tool availability and specialized engineering talent. Relying on optimistic vendor delivery timelines without securing secondary sourcing alternatives is a severe fiduciary failure for any modern technology executive.

Power consumption remains the most ignored risk factor in this entire high-performance computing narrative dominated by Advanced Micro Devices and its market peers. Designing chips that require over 1,000 watts per unit creates an immediate infrastructure crisis for data centers unequipped to handle extreme thermal loads. We advise clients that purchasing this advanced silicon is functionally useless if your hosting facility cannot physically power and cool the deployed server racks.

The strategic gap between designing a chip and securing the specialized packaging capacity required to finalize it remains alarmingly wide across the industry. Advanced Micro Devices relies heavily on limited Taiwanese manufacturing infrastructure, creating immense geopolitical risk that enterprise buyers passively inherit. Operational resilience demands that you factor these regional concentration risks into your corporate hardware lifecycle planning and disaster recovery protocols.

Gross margin guidance of 56% indicates that semiconductor manufacturers will aggressively pass their rising production costs directly onto enterprise consumers. L-Impact Solutions predicts a significant, sustained unit-cost inflation cycle for all enterprise networking and compute hardware over the next twenty-four months. Financial officers must immediately adjust their capital expenditure models to account for these unavoidable hardware premiums and increased operational costs.

The current semiconductor market operates under a false premise that hyperscale cloud providers will absorb all supply chain friction for the end user. In reality, these cloud giants pass down physical hardware constraints in the form of regional instance unavailability and unannounced compute price hikes. Your enterprise architecture must become cloud-agnostic and hardware-flexible to survive these opaque, highly restrictive infrastructure rationing tactics.

We strongly critique the ongoing industry narrative that completely ignores the critical shortage of power management integrated circuits and basic analog controllers. While the market obsesses over advanced $30,000 artificial intelligence chips, production lines frequently halt because of missing two-dollar power regulation components. A sophisticated corporate strategic sourcing strategy must monitor the availability of basic microcontrollers just as closely as premium silicon accelerators.

| Related Analysis: Spirit Airlines $500M Bailout Failure: Pricing Blueprint GVA Q1 Beat 30.4% Margin Crisis: Secure Your Margins Fast XRP $620T Risk: Secure Your Models Now |

Solutions for Enterprise Artificial Intelligence Supply Risks

Securing physical hardware in a supply-constrained market requires enterprise buyers to execute legally binding, multi-year capacity reservation agreements with trusted hardware vendors. You must bypass traditional transactional procurement channels and negotiate directly with original equipment manufacturers to guarantee your position in the fulfillment queue. This strategic sourcing approach transforms hardware acquisition from a reactive operational task into a proactive, powerful corporate asset protection mechanism.

Organizations must implement aggressive dual-sourcing mandates across all critical infrastructure layers to mitigate the risk of vendor-specific manufacturing delays. Utilizing hardware from Advanced Micro Devices alongside competing silicon architectures ensures your data center operations continue even if one specific product line stalls. This architectural flexibility demands early investment in containerized software environments that can seamlessly transition workloads between different underlying processor types.

Managing the extreme thermal loads of modern artificial intelligence processors requires immediate capital investment in advanced direct-to-chip liquid cooling infrastructure. Traditional air-cooled data center environments cannot physically sustain the 60-kilowatt rack densities generated by these next-generation computing clusters. Upgrading your facility cooling capabilities prevents expensive hardware from thermally throttling and destroying your expected financial return on investment.

Financial executives must deploy sophisticated predictive analytics platforms to monitor global semiconductor supply chain anomalies in real time. These data platforms detect early warning signs of component shortages in raw materials like gallium or high-bandwidth memory months before they impact final server deliveries. Leveraging this intelligence allows your procurement teams to accelerate purchase orders ahead of anticipated market crunches and component shortages.

Optimizing your power usage effectiveness is a mandatory operational solution as local utility grids strictly limit data center electricity allocations globally. Implementing artificial intelligence-driven facility management software can reduce non-computing energy waste by up to fifteen% across your infrastructure portfolio. Maximizing power efficiency directly allows you to deploy more revenue-generating compute nodes within your existing hard physical power limits.

Enterprises facing severe hardware delivery delays should strategically leverage specialized cloud instances as temporary bridge solutions for critical workloads. Reserving compute capacity through secondary cloud providers mitigates the risk of stalled internal data center deployments while waiting for physical silicon delivery. This hybrid deployment strategy guarantees project continuity while absorbing the inevitable shocks of the physical global supply chain.

Extending the lifecycle of existing enterprise hardware through targeted maintenance programs provides immediate financial relief from current supply market pressures. Delaying non-essential server refreshes by twelve to eighteen months preserves capital while the semiconductor manufacturing industry resolves its current advanced packaging bottlenecks. This tactical patience prevents your firm from paying massive premium markups during temporary supply shortages and logistics crunches.

Establishing direct relationships with specialized component distributors provides enterprise buyers with critical visibility into the secondary hardware market. When primary original equipment manufacturers fail to meet delivery timelines, these independent distribution channels often hold critical inventory of required networking and compute assets. Maintaining active accounts with these specialized brokers serves as an essential insurance policy against unexpected supply chain failures.

Companies must rewrite their software applications to utilize computational resources more efficiently rather than simply purchasing additional hardware brute force. Code optimization, algorithmic efficiency, and advanced quantization techniques can drastically reduce the amount of physical silicon required to perform complex artificial intelligence tasks. Solving hardware scarcity through software elegance remains the most cost-effective solution for modern enterprise engineering teams facing capacity constraints.

Corporate boards must authorize advanced inventory buffer strategies, shifting away from vulnerable just-in-time global logistics models. Holding strategic reserves of critical networking switches, memory modules, and processing units protects operational continuity during severe geopolitical supply chain disruptions. The carrying cost of this physical inventory is mathematically negligible compared to the massive financial losses incurred during an infrastructure deployment halt.

Prevention Steps for Future Infrastructure Bottlenecks

Preventing future hardware crises requires establishing a dedicated internal supply chain risk committee composed of engineering, finance, and procurement executives. This cross-functional team must continuously evaluate global geopolitical developments and their direct threat vectors to your specific semiconductor dependencies. Institutionalizing this threat assessment protocol ensures your organization reacts to factory closures or export restrictions months faster than your competitors.

Enterprises must design their future data center topologies using modular, vendor-neutral hardware specifications rather than proprietary physical form factors. Standardizing server racks, power delivery, and cooling connections prevents permanent vendor lock-in and allows seamless integration of future semiconductor innovations. This physical abstraction layer guarantees your facility can accept hardware from Advanced Micro Devices or any competitor without requiring massive structural retrofitting.

Securing long-term renewable power purchase agreements is an absolute prerequisite to prevent future operational scaling constraints and grid limitations. Artificial intelligence workloads demand massive baseline power, and relying on spot-market municipal grid electricity exposes your firm to catastrophic pricing volatility. Contracting dedicated solar, wind, or nuclear power generation guarantees cost predictability and secures your facility’s operational license to operate indefinitely.

Organizations must aggressively map their sub-tier supplier networks to identify hidden dependencies on localized material providers or single-point packaging facilities. Understanding exactly where your server components are manufactured allows you to preemptively pivot orders when specific global regions experience severe disruption. Complete supply chain visibility prevents your strategic initiatives from being derailed by an obscure factory issue deep within the manufacturing ecosystem.

Financial planning departments must decouple hardware acquisition budgets from traditional annual corporate budgeting cycles to navigate market volatility effectively. Establishing continuous, rolling capital expenditure funds allows procurement teams to secure strategic hardware inventory immediately when opportunistic market conditions arise. This financial agility prevents artificial internal administrative roadblocks from interfering with critical, time-sensitive infrastructure acquisitions.

You must integrate hardware availability metrics directly into your software engineering development lifecycle and agile project planning phases. Product managers must verify physical compute availability before committing to artificial intelligence feature releases to prevent embarrassing public service delays. Synchronizing software ambition with hardware reality eliminates the operational friction that typically destroys enterprise technology timelines.

Developing strong localized talent pipelines for data center engineers and thermal management specialists prevents future operational bottlenecks. Deploying advanced silicon requires highly specialized personnel to manage complex liquid cooling manifolds and high-density power distribution systems safely. Funding local university partnerships and specialized corporate training programs ensures your facilities operate efficiently regardless of external labor market constraints.

Contracts with original equipment manufacturers must include severe, financially devastating penalty clauses for missed delivery timelines and broken promises. Forcing vendors to share the financial risk of supply chain delays incentivizes them to prioritize your hardware allocations over less aggressive clients. This legal posturing establishes your firm as a priority tier-one customer in the eyes of major global hardware distributors.

Companies must actively participate in open-source hardware consortiums to drive industry-wide standardization of critical computing infrastructure components. Contributing to shared specifications reduces the broader industry reliance on proprietary, single-source semiconductor architectures that heavily restrict market competition. Supporting open ecosystems directly dilutes the monopolistic pricing power currently held by top-tier silicon designers and fabricators.

Conducting bi-annual infrastructure disaster simulation drills forces your organization to test its theoretical supply chain resilience against realistic market shocks. Simulating a total regional fabrication shutdown reveals practical weaknesses in your secondary sourcing strategies and emergency cloud migration protocols. These rigorous, data-driven stress tests transform theoretical prevention strategies into verified, battle-ready corporate capabilities capable of surviving market turbulence.

L-Impact Solutions Key Takeaway

The massive $10.25 billion revenue surge reported by Advanced Micro Devices represents a dangerous market illusion where financial success masks severe physical infrastructure vulnerabilities. L-Impact Solutions firmly asserts that enterprise leaders who blindly trust vendor delivery roadmaps will face catastrophic operational failures within the next twenty-four months. You must instantly transform your procurement division into a strategic defense asset capable of navigating extreme geopolitical and physical supply chain volatility.

The artificial intelligence revolution is no longer constrained by software innovation, but entirely dictated by global power grid limits and specialized semiconductor packaging capacity. Your competitive advantage moving forward depends entirely on mastering physical data center thermal dynamics and executing ruthless dual-sourcing hardware strategies. Companies that fail to internalize this harsh physical reality will inevitably watch their digital transformation initiatives collapse under the weight of unavailable silicon.

FAQs:

How will AMD’s 56% gross margin guidance and rising fabrication costs impact enterprise hardware budgets?

Organizations that don’t proactively adjust capex forecasts are heading toward budget shocks, as vendors will inevitably pass escalating production costs directly to buyers.

What risks arise from AI chips representing <0.2% of global semiconductor volume despite a $975B industry size?

This extreme concentration creates systemic fragility, and firms not modeling component-level dependencies will experience cascading delays from even minor supply disruptions.

How should businesses respond to hyperscalers investing $185B in capex while mid-market firms face shrinking hardware allocations?

Relying on spot procurement is no longer viable, and companies that fail to secure priority vendor partnerships will be structurally locked out of critical compute capacity.

What does the projected 1,050 TWh data center power demand by 2026 mean for deploying high-density AI infrastructure?

Enterprises ignoring energy constraints are making a critical strategic error, as power availability—not chips—will ultimately dictate whether their AI investments deliver any ROI.

How can enterprises sustain AI scaling when AMD’s $10.25B revenue surge and 57% data center growth outpace semiconductor supply capacity?

Most firms dangerously underestimate supply fragility, and without multi-year capacity contracts and dual-sourcing, their AI expansion plans will stall under predictable hardware shortages.