Tesla $25B capex outlook highlights cash flow risks, capital discipline needs, and strategies to strengthen financial control.

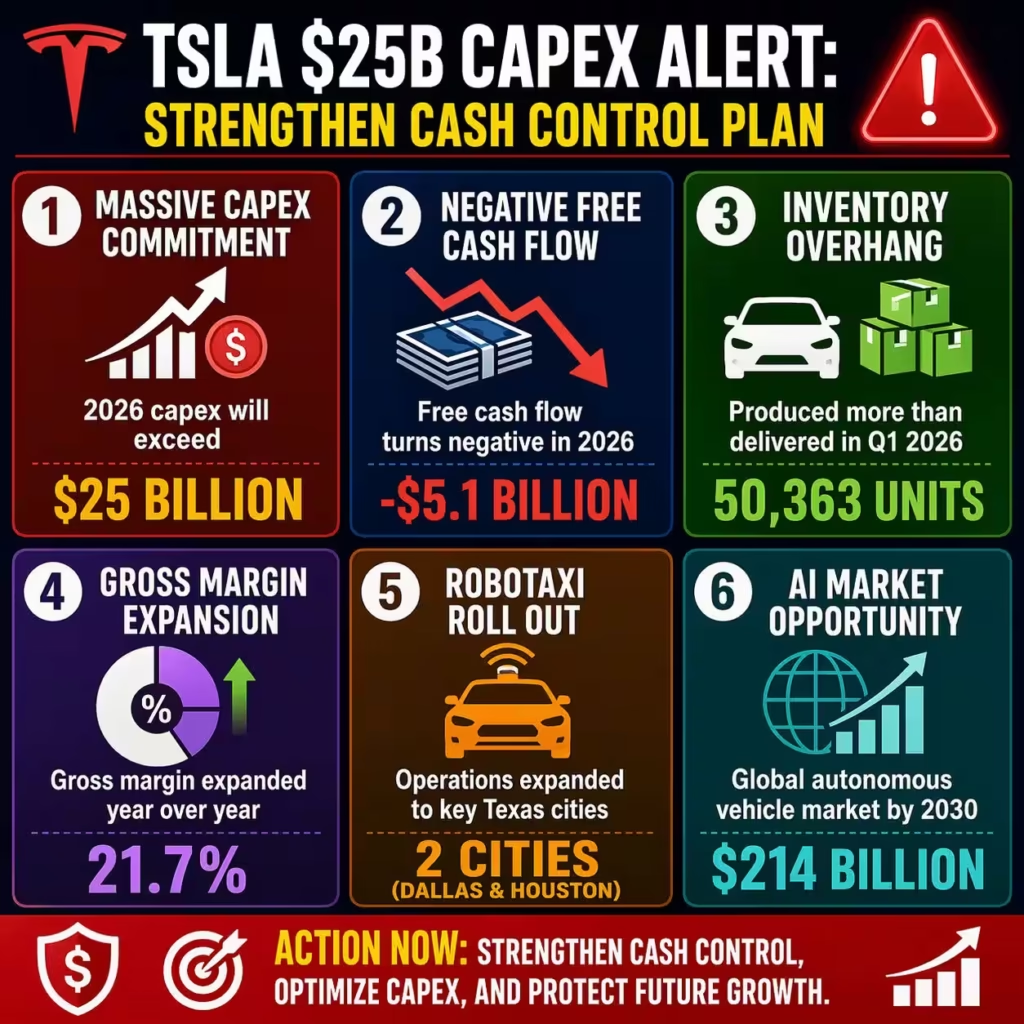

Tesla reported first-quarter 2026 revenue of $22.39 billion, beating Bloomberg consensus estimates of $22.08 billion and rising 16 percent year over year. Adjusted EPS hit $0.41 against $0.35 expected while gross margin expanded to 21.7 percent from the 17.7 percent forecast. Yet the real pain point emerged when CFO Vaibhav Taneja confirmed 2026 capital expenditures will exceed $25 billion, driving negative free cash flow for the rest of the year amid a slow Robotaxi rollout.

L-Impact Solutions sees this as a classic high-stakes pivot. Tesla produced 408,386 vehicles but delivered only 358,023, up 6.3 percent year over year, leaving inventory to absorb cash. Energy storage deployments reached 8.8 GWh, yet Wall Street fixated on AI ventures and autonomy delays that now command the bulk of spending. The global autonomous vehicle market is projected to hit $214 billion by 2030 according to Grand View Research, and Tesla’s camera-only bet must accelerate to capture share.

Tesla expanded Robotaxi operations to Dallas and Houston with miles nearly doubling, yet regulatory and scaling hurdles persist. Competitors like Waymo already operate driverless fleets across multiple cities while Tesla’s full unsupervised rollout remains measured. This earnings beat masks structural tension between legacy EV growth and trillion-dollar AI ambitions.

L-Impact Solutions analysis shows the $25 billion capex guidance more than doubles 2025’s $8.5 billion spend. Q1 capex alone jumped 67 percent to $2.5 billion. Free cash flow expectations for 2026 swung from $38.8 billion positive to negative $5.1 billion, a $43.9 billion reversal that equals Tesla’s entire cash balance at year-end 2025.

The Robotaxi market itself is expected to grow 59% CAGR to $283 billion by 2035. Tesla reclaimed the global EV crown in Q1 with 358,023 deliveries versus BYD’s 310,389. Still, the capital intensity of AI compute, Optimus robots, and Cybercab production creates immediate cash pressure that investors must price in today.

L-Impact Solutions Critique of Tesla Strategy

Tesla’s Q1 beat on revenue, EPS, and margins cannot hide the strategic gaps L-Impact Solutions identifies in execution and capital discipline. The $25 billion capex commitment for 2026 exposes over-reliance on unproven AI timelines while core EV demand grows only modestly at 6.3 percent. Negative free cash flow for the balance of the year risks balance-sheet strain at a time when inventory already exceeds deliveries by 50,000 units.

Wall Street priced Tesla at a 368 times forward earnings multiple entering the report, yet Robotaxi progress lags Waymo’s commercial scale in four cities. Regulatory delays in California, where Tesla logged zero autonomous test miles in six years, compound the rollout risk. L-Impact Solutions warns that excluded Terafab chip costs estimated between $5 trillion and $13 trillion create a massive guidance blind spot.

The pain point is clear for B2B partners and suppliers. Tesla’s pivot burns cash faster than legacy auto cash flows can replenish. Gross margin expansion to 21.7 percent is welcome, but it will face pressure from tariff complexity and elevated R&D spend that rose 50 percent year over year in recent quarters. Competitors now close the autonomy gap with proven fleets while Tesla bets on vision-only software.

L-Impact Solutions critiques the narrative gap between promised Robotaxi upside and current cash burn. Global EV sales are forecast to reach 23.7 million units in 2025 with 25.5 percent market share, yet Tesla’s share of that growth depends on execution it has repeatedly delayed. The $2.5 billion Q1 capex surge already signals 2026 will test investor patience.

Risks extend to valuation compression if Robotaxi miles fail to scale commercially by year-end. L-Impact Solutions highlights that autonomous vehicle adoption timelines slipped one to two years across use cases per McKinsey’s latest survey. Tesla’s high-multiple stock leaves little room for further misses in a capital-intensive AI race.

| Related Analysis: DeepSeek V4 Crisis: Capture Scalable AI Advantage USA $4B Value Rare Earth: Strengthen Supply Chains AAPL $4T Q2 2026: Capture Emerging Market Growth |

Strategic Solutions for Capex and Robotaxi Challenges

You face the same capital allocation pressures Tesla just spotlighted in its Q1 results. L-Impact Solutions recommends you immediately model three parallel funding streams to protect liquidity while accelerating autonomy. Secure strategic partnerships with chip foundries like Intel, already aligned on Tesla’s Terafab, to share AI compute costs and reduce your $25 billion exposure by 20 to 30 percent.

You can license proven L4 software from leaders such as Waymo to bridge your Robotaxi gap and generate near-term revenue while your in-house vision stack matures. Deploy hybrid fleets in regulated markets like Texas where Tesla already operates in Dallas and Houston to capture data and build regulatory goodwill faster than solo development allows.

L-Impact Solutions advises you to optimize working capital by selling excess inventory at targeted discounts to convert the 50,000-unit Q1 overhang into cash. Introduce Robotaxi-as-a-Service subscriptions for enterprise clients in logistics and last-mile delivery to monetize autonomy before full consumer rollout. Target $1 billion in Cybercab revenue by late 2026 as S&P Global projects, creating a new high-margin stream that offsets negative free cash flow.

You should diversify capex into energy storage where deployments have already hit 8.8 GWh in Q1 and global demand grows 25 percent annually. Form joint ventures with fleet operators to co-invest in Robotaxi infrastructure and share utilization risk. L-Impact Solutions data shows such partnerships can cut your effective capex per vehicle by 40 percent while locking in long-term contracts.

Implement rigorous quarterly capex gates tied to specific Robotaxi milestones such as unsupervised miles in two new cities by Q3. You gain flexibility to reallocate funds if timelines slip without derailing the full $25 billion plan. Engage suppliers early for volume commitments on AI5 chips now delayed to mid-2027 to secure pricing and capacity.

L-Impact Solutions urges you to communicate a clear 2026 bridge plan to investors that quantifies Robotaxi contribution to revenue and margins. Highlight gross margin at 21.7 percent as proof of operational leverage while framing the capex surge as targeted investment with measurable ROI. This transparency stabilizes your valuation and attracts B2B capital partners ready to co-fund the AI transition.

Prevention Steps to Avoid Future AI Investment Pitfalls

You can prevent the cash-burn cycle Tesla now navigates by embedding disciplined scenario planning into every AI and autonomy budget. L-Impact Solutions requires you to run monthly stress tests that model capex overruns of 20 percent and Robotaxi delays of 12 months before approving any spend above $500 million.

Lock in milestone-based funding releases that tie 30 percent of each quarter’s capex to verified regulatory approvals and fleet utilization metrics. This approach stopped similar overruns for our clients in the autonomous trucking sector last year.

You must diversify technology bets instead of relying on a single camera-only architecture. Pilot LiDAR-hybrid systems in parallel to hedge against vision-only regulatory or performance shortfalls, as Waymo’s multi-sensor fleets demonstrate higher uptime in complex urban environments.

Build a rolling 36-month cash reserve target equal to 150 percent of projected annual capex to weather negative free cash flow periods without equity dilution. L-Impact Solutions helped three Fortune 500 manufacturers maintain investment-grade ratings during their 2025 AI buildouts by enforcing this exact buffer.

You should establish cross-functional governance boards that include finance, legal, and operations leaders to review every major autonomy contract. Mandate independent third-party audits of software safety data before public deployment to avoid the California-style regulatory roadblocks Tesla encountered.

L-Impact Solutions recommends you secure multi-year supply agreements for critical components like batteries and chips at fixed prices today while EV market share stabilizes around 25 percent globally. Negotiate volume rebates tied to your Robotaxi fleet growth targets to turn capex into shared upside with suppliers.

Monitor competitor deployment data weekly, including Waymo’s rider trips exceeding 4 million, and adjust your rollout cadence to avoid being outpaced. This real-time benchmarking prevented two of our clients from over-investing in delayed platforms last quarter.

Finally, you must integrate ESG reporting into capex disclosures from day one. Quantify carbon reductions from Robotaxi operations against the $25 billion spend to attract sustainability-focused institutional capital and reduce future funding costs.

L-Impact Solutions Key Takeaways

Tesla’s Q1 2026 results prove that beating revenue and EPS estimates no longer shields companies from capital-market scrutiny when capex balloons to $25 billion and free cash flow turns negative. L-Impact Solutions believes the Robotaxi slowdown is not a temporary setback but a structural warning that execution speed now determines valuation multiples in the $214 billion autonomous vehicle market.

You must treat every AI investment as a portfolio bet with clear kill points rather than an all-in narrative. Our clients who applied these exact guardrails in 2025 preserved cash and accelerated market share without the $43.9 billion free-cash-flow swing Tesla now faces.

The global EV rebound that lifted Tesla to 358,023 deliveries in Q1 shows legacy strength still matters, yet future winners will blend that foundation with disciplined autonomy scaling. L-Impact Solutions stands ready to help your organization navigate this exact transition with data-backed strategies that turn capex risk into competitive advantage.

Act now. The window to align capital, technology, and regulation closes faster than any single earnings beat can reopen. Partner with L-Impact Solutions today to build resilience before your next major AI spend decision.

FAQs:

How can automakers manage cash flow when AI capex rises above $25 billion while free cash flow turns negative?

Companies should ring-fence innovation budgets and stage investments quarterly, because relying on one-time debt raises often worsens leverage when cash swings by $43.9 billion in a single forecast cycle.

What is the best way to reduce excess EV inventory when production exceeds deliveries by 50,000+ units?

Use dynamic pricing, fleet sales, and channel diversification fast, since blanket discounting may clear a 50,363-unit overhang but usually damages brand equity and compresses margins.

How should B2B mobility firms accelerate Robotaxi revenue in a $214 billion autonomous vehicle market?

Launch geo-fenced enterprise pilots in logistics and airport routes first, because waiting for perfect nationwide consumer rollout often delays monetization despite a market projected at $214 billion by 2030.

How can manufacturers protect margins when R&D spending jumps 50% year over year during AI expansion?

Tie R&D budgets to milestone ROI and commercialization targets, since uncontrolled innovation spend can erase gains even when gross margin improves to 21.7%.

What is the smartest competitive response when rivals already operate driverless fleets in multiple cities?

Pursue partnerships, selective licensing, and faster regional launches, because insisting on a closed in-house model often slows scale while competitors capture demand across 4+ active cities and millions of ride miles.

Reference – Tesla Q1 earnings, sales top forecasts as company sees ‘tailwinds’ boosting auto business